This company generates the power to see sustainable profitability at Uniform ROA of 10%, not 6%

As the world reopens, global demand for oil is picking back up again. However, the Organization of the Petroleum Exporting Countries (OPEC) is maintaining its decision to keep oil production at a moderate level, effectively increasing oil prices as supply runs low.

This power-generating company is currently operating renewable energy plants to source alternative energy for the Philippines. Though as-reported metrics make it look like the company is just breaking even in a market dominated by traditional fossil fuels, Uniform return on assets show the company has been doing better.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In July 2020, investment firm Kohlberg Kravis Roberts & Co. (KKR) acquired up to PHP 9.6 billion worth of outstanding shares of First Gen Corporation (FGEN:PHL), representing 11.9% economic interest of the company. KKR had seen potential in the Philippine renewable and clean energy markets, and it wanted to be a part of that growth opportunity.

Then a few weeks ago, KKR decided to buy 7.3% of the company’s outstanding common share capital, resulting in nearly 20% of First Gen’s total ownership.

However, this latest transaction posed a concern for First Gen’s place in the Philippine Stock Exchange index (PSEi).

Current guidelines require companies to maintain a public float level of 15% of their outstanding common share that is openly accessible and tradable in the market. With KKR’s additional acquisition of shares, it’s unlikely that First Gen would meet that requirement.

So in a third index review for the year, First Gen was removed and home improvement retailer Wilcon Depot, Inc. (WLCON:PHL) was added to the PSEi.

PSEi composition aside, First Gen’s growth opportunities remain as rising fuel prices and the shift to more sustainable living pressure companies to invest less in coal and other similar power plants.

For instance, the Philippine government enacted a Feed-in Tariff (FiT) scheme for renewable energy that will give renewable energy developers a fixed price for the purchase of their power generation over a period of time. This aims to advance the development of emerging renewable energy resources to lessen the dependence on imported fossil fuels.

First Gen is particularly positioned to benefit from this renewable energy demand in the long term through its ownership of Energy Development Corporation, the largest geothermal power producer in the country.

However, even with significant tailwinds on its side, First Gen has recently had its fair share of challenges, mainly due to the pandemic.

First Gen’s electricity sales declined by 15% in 2020 to PHP 91.2 billion from PHP 111.8 billion in 2019 due to government restrictions for businesses and operations. Its natural gas, geothermal/wind/solar, and hydro segments were all negatively impacted by the lower average WESM (wholesale electricity spot market) prices, at worst to a third of 2019 prices.

Furthermore, if First Gen continues to experience supply constraints from the Malampaya natural gas field, it could be facing its own supply issues to Meralco.

The Manila Electric Company (MER:PHL), also known as Meralco, currently has a 25-year power purchase agreement with First Gen’s Sta. Rita Power Plant under First Gas Power Corporation. This means Meralco is contractually obligated to purchase a minimum energy quantity of natural gas from First Gen.

With Meralco driving 57% of First Gen’s electricity sales, the reopening of the economy will most likely help First Gen’s returns for shareholders in the short term as well.

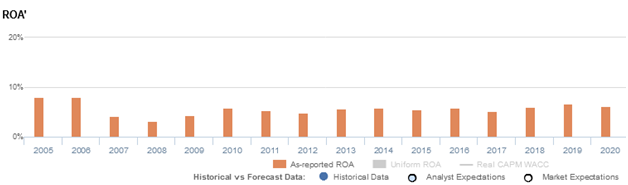

Looking at the as-reported metrics, First Gen has had stable returns near cost-of-capital levels, implying that the firm has generated little economic value for its stockholders in the past decade.

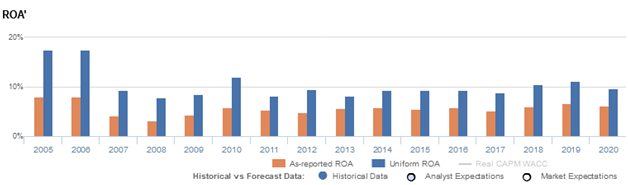

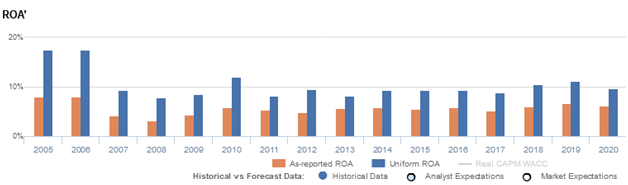

However, looking at First Gen’s real economic profitability, we see that the firm has actually been improving in the last ten years. In fact, in the past decade, it has been sustaining levels almost double as-reported ROA levels.

Historically, one of the largest distortions for First Gen comes from the treatment of minority interest expenses or the income attributable to the non-controlling interests of a company’s subsidiaries.

The Philippine Financial Reporting Standards (PFRS) allows minority interest expense to be recognized under operating cash flow, leading people to incorrectly think that it is essential to the firm’s core operations.

In reality, it should always be classified as a financing cash flow. Minority shareholders provide capital to the subsidiary in exchange for a piece of the company’s profits. As a result, minority interest expense should not be subtracted from revenue when calculating a company’s real core earnings.

In 2020, First Gen recognized PHP 118.0 million in minority interest expense, resulting in a PHP 278 million net profit and a 6% as-reported ROA. Adding this back alongside the many other adjustments Valens makes, the company should actually be recognizing PHP 398 million in Uniform earnings and a 10% Uniform ROA.

First Gen’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

First Gen’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 6% in 2020, significantly lower than Uniform ROA of 10%.

Moreover, since 2008, Uniform ROA has expanded from 8% to 10% in 2020, while as-reported ROA has only improved from 3% to 6% over the same timeframe. The as-reported metrics are misleading investors’ perception of the firm’s historical profitability trend.

After falling from 18% levels in 2005-2006 to 8% in 2008, Uniform ROA gradually improved to 10%-11% levels in 2018-2020, excluding a 12% outperformance in 2010.

First Gen’s asset turns are more efficient than you think

Trends in Uniform ROA have been driven by trends in Uniform asset turns. Since 2005, as-reported metrics have significantly understated First Gen’s asset utilization, a key driver of profitability.

Uniform turns improved from 0.7x in 2005 to 1.1x in 2006, before falling back to 0.6x in 2007 and rebounding to a peak of 1.2x in 2012. Thereafter, Uniform turns declined to 0.5x-0.6x levels from 2014-2019, before fading to 0.4x in 2020.

Meanwhile, after dropping from 0.6x highs in 2005-2006 to a low of 0.2x in 2007, as-reported asset turnover recovered to 0.5x levels in 2009-2012. Then, as-reported asset turnover compressed to 0.3x-0.4x levels through 2020.

As-reported metrics have been making First Gen appear to be a less efficient business than real economic metrics highlight.

SUMMARY and First Gen Corporation Tearsheet

As our Uniform Accounting tearsheet for First Gen Corporation (FGEN:PHL) highlights, the company trades at a Uniform P/E of 18.7x, below the global corporate average of 24.3x, and its historical P/E of 10.9x.

Low P/Es require low EPS growth to sustain them. In the case of First Gen, the company has recently shown a 7% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, First Gen’s sell-side analyst-driven forecast is to see Uniform earnings grow by 31% and 4% by 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify First Gen’s PHP 28.40 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to decline 15% annually over the next three years. What sell-side analysts expect for First Gen’s earnings growth is well above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 2x above the long-run corporate average. However, cash flows and cash on hand fall below total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 410bps above the risk free rate. Together, this signals a high credit and a moderate dividend risk.

To conclude, First Gen’s Uniform earnings growth is above its peer averages, but currently trades in line with its average peer valuations.

About the Philippine Market Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com