This home improvement retailer’s focus on building its growth strategy enabled it to reach a Uniform ROA of 10%, not 5%

This home improvement retailer replaced First Gen Corporation (FGEN:PHL) on the Philippine Stock Exchange index (PSEi) on Monday, less than two months after the index had just undergone its semi-annual review.

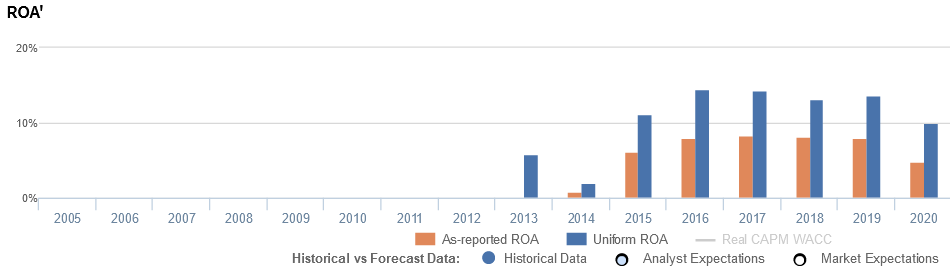

Though this retailer has been executing its growth strategy, and most recently its digital initiatives, well over the years, as-reported metrics show that the company isn’t doing that well at all. Uniform Accounting, on the other hand, reveals the company has actually achieved more than 10% return on assets (ROA) despite the challenging environment.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

A stock market index is an important indicator of a country’s overall market condition.

In the Philippines, we have the Philippine Stock Exchange Index PSEi, which consists of 30 of the largest publicly traded companies that meet the minimum free float level and liquidity and capitalization criteria.

Twice a year, the PSEi undergoes a rebalancing review that checks if its constituents still meet those requirements.

The second—and presumably final—review for this year was in August. As we’ve previously discussed, liquor-maker Emperador (EMP:PHL) and Consunji-led conglomerate DMCI Holdings (DMC:PHL) were replaced by recently public Converge (CNVRG:PHL) and Ayala-led AC Energy (ACEN:PHL).

Imagine the market’s excitement when the Philippine Stock Exchange announced a third review only two months after: The Lopez-led First Gen Corporation (FGEN:PHL) will be replaced by home improvement retailer Wilcon Depot, Inc. (WLCON:PHL).

The former’s removal was due to the tender offer transaction of US-based private equity firm Kohlberg Kravis Roberts & Co (KKR), which reduced First Gen’s public float.

Since the announcement, the inclusion of Wilcon Depot has caused a stir in the stock market as the company’s stock price increased by 8.5% on Thursday. That aside though, the company has already been doing well for the past few years.

In 2020, Wilcon Depot took advantage of pandemic-related opportunities and recalibrated its strategies to catch up with emerging trends.

Specifically, work-from-home arrangements increased the demand for retail home improvement products, which kept the company’s business profitable. On top of that, thanks to its continued efforts on its online store, revenues only declined 8% from PHP 24.5 billion in 2019 to PHP 22.6 billion in 2020.

Wilcon Depot was also able to continue with its expansion initiatives, increasing the capital expenditures budget by 45% as compared to last year.

As a result, it managed to open five branches during the first three quarters of the year, while four more are expected to be operational within the next few months, which makes it a total of 72 stores by the end of 2021.

All in all, Wilcon Depot’s ability to improve and grow its business enabled the company to become one of the biggest retailers in the country.

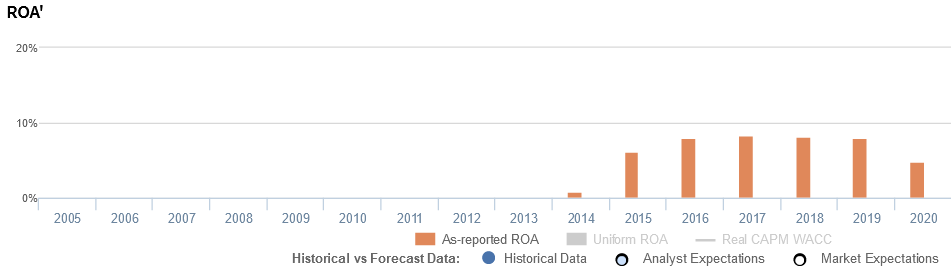

However, as-reported data seems to show that these initiatives weren’t enough to represent sustainable profitability, with ROAs only reaching 5% in 2020.

In reality, Wilcon Depot’s strong focus on store expansion and retail strategy actually proved that the company actually produced steady profitability, with Uniform ROAs achieving more than 10%.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

Specifically, in 2020, Wilcon Depot recorded interest costs at PHP 429 million. Adding back this expense because it is not an operating expense, along with many other necessary adjustments made by Valens, leads to a PHP 1.8 billion net income and a 10% Uniform ROA, higher than its PHP 1.4 billion as-reported net loss and immaterial as-reported ROA.

Wilcon’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that Wilcon’s profitability is higher than what real economic metrics highlight in all years.

In reality, Wilcon’s true profitability has consistently been higher than its as-reported ROA since 2013. For example, as-reported ROA was 5% in 2020, but Uniform ROA is displaying much stronger profitability at 10%.

Historically, as-reported ROA has improved from a low of 1% in 2014 to 8% levels in 2016-2019, before compressing to 5% in 2020. Meanwhile, Uniform ROA expanded from 2% in 2014 to 13%-15% levels in 2016-2019, before declining to 10% in 2020.

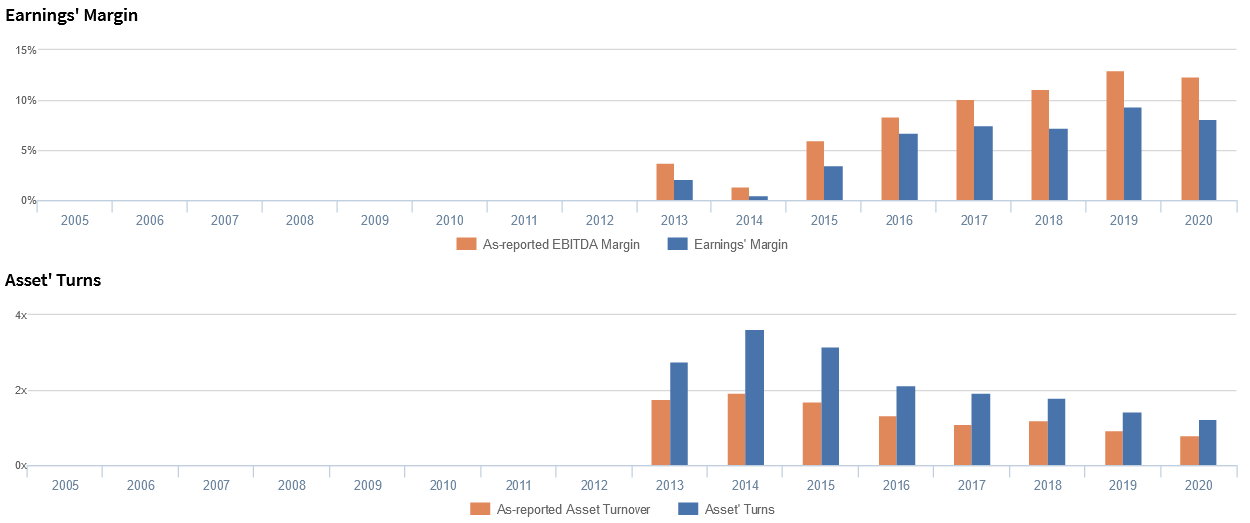

Wilcon’s earnings margin is much weaker than you think, but its Uniform asset turns make up for it

Trends in Uniform ROA have been driven by trends in Uniform earnings margin, coupled with declining Uniform asset turns.

Uniform margins expanded from 2% in 2013 to a high of 9% in 2019, before compressing to 8% in 2020. Meanwhile, after improving from 2.8x in 2013 to 3.6x in 2014, Uniform turns declined to 1.2x in 2020.

At current valuations, the market is pricing in expectations for both Uniform margins and Uniform turns to reach new peaks.

SUMMARY and Wilcon Depot Tearsheet

As our Uniform Accounting tearsheet for Wilcon Depot, Inc. (WLCON:PHL) highlights, the company trades at a Uniform P/E of 53.1x, above the global corporate average of 24.3x and its historical P/E of 36.5x.

High P/Es require high EPS growth to sustain them. In the case of Wilcon Depot, the company has recently shown a 30% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Wilcon Depot’s sell-side analyst-driven forecast is to see a Uniform earnings growth of 57% and 25% in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Wilcon Depot’s PHP 34.95 stock price. These are often referred to as market-embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 29% annually over the next three years. What sell-side analysts expect for Wilcon Depot’s earnings growth is above what the current stock market valuation requires in 2021, but below its requirement in 2022.

Furthermore, the company’s earning power is 2x the long-run corporate average. In addition, cash flows and cash on hand are 2x their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Wilcon Depot’s Uniform earnings growth is in line with its peer averages, but currently trades well above its average peer valuations.

About the Philippine Market Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com