This company’s products and marketing strategies were game changers, leading to one of the bestselling consoles and a Uniform ROA of 12%, not just 2%!

Playing video games has always been a favorite pastime, but its audience grew even wider during the pandemic when everybody had to stay at home. Video game platforms have come a long way, from being available only at arcades to becoming a family activity and to becoming a popular online activity whether through computers or mobile phones.

This company, with its technology and marketing strategy, was able to attract its target demographic, making its product one of the most successful video game consoles in the world.

Uniform Accounting indicates that this company’s Uniform return on assets (ROA) deserves far more recognition than it is getting since its profitability is higher than what as-reported metrics show.

Also, below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Most success stories begin with rejection.

For this company, it all started with a failed partnership.

This company was initially in talks for a collaboration with Nintendo, a prominent video game company, to create a new gaming console. However, this venture did not push through because Nintendo backed out.

This company decided to do it alone, releasing its own gaming console.

Sony Corporation is a Japanese conglomerate that manufactures consumer electronics products. The company is a leading player in the segments it operates such as Game & Network Services, Music, Pictures, and Electronics Products & Solutions.

In 1994, Sony launched the PlayStation in Japan, presenting its games with real-time 3D graphics. The console was then released in the U.S. in 1995. Along with its more advanced technology is better aesthetics for the console, with its games stored in much sleeker and more compact black CDs, making the game cartridges look outdated.

Sony’s PlayStation wasn’t just game-changing thanks to the technology behind it, but also because of the branding and marketing strategies that the firm employed.

While Nintendo’s games were mostly for kids, Sony targeted young adults for PlayStation.

At the time of PlayStation’s release, the young adult market looked like an underserved if not ignored market. This demographic played with Nintendo’s games when they were kids, but did not have a lot of game options as they grew up. This was the market Sony wanted to serve.

For Sony to capture its target market, it released advertisements like “Mental Wealth” and “Double Life” in the UK, which weren’t your run-of-the-mill kind of advertising for the gaming industry. These ads captured the essence of gaming and the experiences that PlayStation has to offer.

Sony sought to foster a deeper connection with its consumers by tapping underground culture, sponsoring extreme sports events and music festivals.

For example, in the mid-1990s, PlayStations were lined in the chillout rooms of a popular multimedia business/nightclub in London called “Ministry of Sound.” By doing this, Sony associated its gaming console to rave music that was on mainstream airwaves during that time, making its presence wider to its target consumers.

For decades, video games were labeled as a just-for-kids entertainment or only for the geeks, but Sony changed that and made gaming stylish, edgy, and cool with the PlayStation.

Today, video games have become one of the more common hobbies, even more so now in the pandemic. There is a wide variety of games offered from different genres that suit the liking of different gamers.

In 2015, Sony outlined a new corporate strategy that focused more on its “growth drivers”. This comprises the segments that are believed to continue to be profitable for Sony in the future, including the PlayStation franchise and Sony Pictures Entertainment. Sony believed that aggressive capital investment in its growth drivers would generate better sales growth and profit expansion for the company.

The video game console industry has always been about finding that competitive advantage that users would be drawn into. Specifically, avid gamers have been keen on looking at console specs that maximize their gaming experience.

Sony has historically been successful in selling its PlayStation line. On June 11, 2020, the company announced the release of PlayStation 5 with new promised features, which is predicted to sell at least 4.6 million units in only its first year, compared to PlayStation 4 that sold 4.2 million units in its first year.

Although Sony has been constantly updating its strategies to effectively adapt to changes in the market, as-reported metrics do not show its REAL profitability.

Sony’s real economic profitability is better reflected with Uniform Accounting adjustments, which show its TRUE earning power.

One metric that causes distortions in as-reported ROAs is its amortization expense.

Amortization expense is generated from the company’s use of intangible assets in a given reporting period. It is a non-cash expense that is spread throughout the intangible asset’s useful life. As a non-cash expense, it does not represent an actual cash outflow.

Deducting amortization expense from the company’s revenues distorts its profitability because there is no actual cash flow that happens when amortization is charged.

Adding back amortization expense is necessary to convert the company’s net income into actual cash flows.

After amortization expense and other significant adjustments are made, Sony’s Uniform ROA is at 12% in 2020, which is much stronger than its as-reported ROA of 2%.

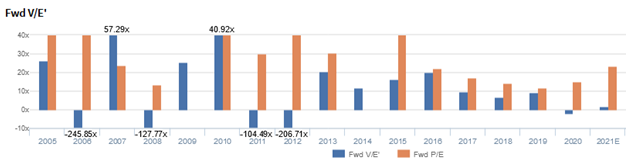

Sony Corporation is cheaper than you think

Sony Corporation currently trades at a 1.7x Uniform P/E (blue bars), which is significantly cheaper than the as-reported P/E of 23.3x, and is much lower than market averages.

At these levels, the market is pricing in expectations for Uniform ROA to drop to 1% in 2025, accompanied by 2% Uniform asset growth.

However, analysts have less bearish expectations, projecting Uniform ROA to only compress to 11% in 2021, with a 3% Uniform asset growth.

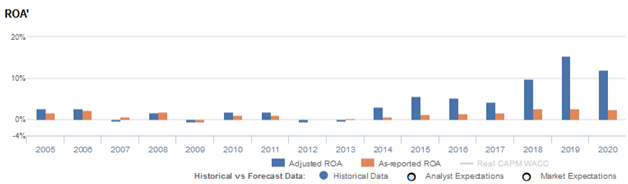

Sony Corporation is more profitable than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Sony’s Uniform ROA has actually been higher than its as-reported ROA in the past seven years. For example, Uniform ROA was 12% in 2020, which is 6x its as-reported ROA of 2%. When Uniform ROA peaked at 16% in 2019, as-reported ROA was just at 3%.

Since 2014, the company’s Uniform ROA has improved from 3% to 12%, while as-reported ROA has increased only from 1% to 2% in the same time frame.

From 3% in 2005, Uniform ROA gradually fell to -1% in 2012, before recovering to 6% in 2015. It then peaked at 16% in 2019, before trending back to 12% in 2020.

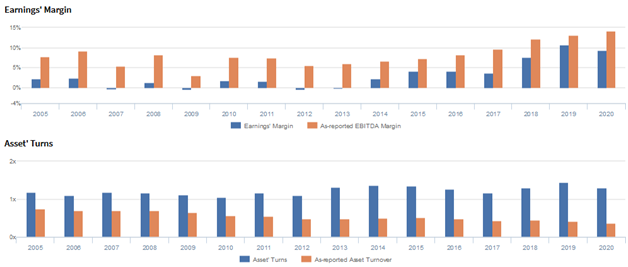

Sony Corporation has weaker Uniform earnings margins than you think, but its robust Uniform asset turns make up for it

Movement in Uniform ROA has been driven by trends in Uniform earnings margins, and to a lesser extent, by Uniform asset turns, with peaks and troughs lining up with that of Uniform ROA.

From 2% in 2005, Uniform earnings margins gradually fell to -1% in 2012, before rebounding to 4% in 2015. It then increased further to 11% in 2019, before declining back to 9% in 2020.

Meanwhile, Uniform asset turns trended at 1.1x-1.2x in 2005 to 2009 before declining to 1.0x in 2010. It then stayed at 1.2x-1.3x levels in 2013 to 2016, before peaking at 1.4x in 2019 and falling again to 1.3x in 2020.

SUMMARY and Sony Corporation Tearsheet

As the Uniform Accounting tearsheet for Sony Corporation (6758:JPN) highlights, the Uniform P/E trades at 1.7x, which is below the corporate average valuation levels and its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Sony, the company has recently shown a 16% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Sony’s sell-side analyst-driven forecast is an 18% earnings shrinkage in 2021, followed by a 22% growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Sony’s JPY 8,280 stock price. These are often referred to as market embedded expectations.

Sony can have Uniform earnings shrink by 41% in the next three years and still justify current prices. What sell-side analysts expect for Sony’s earnings is above what the current stock market valuation requires in 2021 and 2022.

The company’s earning power is 2x the corporate average. Also, cash flows are more than 2x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Sony’s Uniform earnings growth is in line with its peer averages in 2021. Additionally, the company is trading below its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com