This giant telco’s as-reported margin shows the pandemic’s limited impact, and its TRUE margins agree on the direction, not on the level

Thanks to this company’s mobile service offerings, a lot of businesses were able to adapt to the changes in consumer behavior during the pandemic. This allowed smaller businesses without their own digital payment system to continue operations during strict quarantine restrictions.

With this company’s continued focus on capitalizing on its growth opportunity, as-reported metrics suggest that its effort paid off, but Uniform accounting tells a different story.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Financial inclusion, or the effective access of financial services to vulnerable sectors, has been one of the Bangko Sentral ng Pilipinas (BSP) mandates to improve Filipinos’ standard of living.

When individuals or businesses have access to more legitimate credit sources, they are able to contribute more to an economy’s growth whether through spending more or expanding their businesses.

However, as of 2019, 51 million Filipinos remain unbanked because of poverty, reluctance to open a bank account, or lack of required documents. This means 71% of the total adult population in the Philippines does not have the ability to access credit from banks or most financial institutions.

Fortunately, the lack of a bank account is no longer a deterrent in transacting or doing business with others.

67 million out of the 73 million Filipino mobile users have internet access, presenting an opportunity for alternative payment or fund transfer services. This development is something companies like Globe Telecom (GLO:PHL) are taking advantage of.

In our previous article, we mentioned that the company’s sales might increase from 2020 and beyond as a lot of people were forced to work from home. Sure enough, Globe’s home broadband business revenue increased by 23% in 2020, cornering 55% of the market share vs 48% in 2019.

It’s not just Globe’s broadband services that have benefited from more people staying at home. Its mobile data services revenue also improved markedly during the pandemic thanks to GCash.

Though Globe launched GCash as early as 2004, consumer adoption was slow as most Filipinos still preferred cash payments versus transferring money, paying bills, and settling loans with just a simple text message.

In order to attract more people to use its services, Globe launched its free mobile app launch for GCash eight years later.

However, cash still remained king until 2019. Mobile payment adoption only really took off in 2020 after the pandemic forced people to resort to cashless payments.

Today, Mynt, the portfolio company that handles GCash, was able to double its user base of 20 million before the pandemic to a whopping 40 million as of May 2021.

In order to further expand its reach, GCash also partnered with different companies. For example, its partnership with Philippines’ AirAsia, a low-cost airline based in Manila, enables flyers to use GCash as a form of payment for the airline’s services going forward.

On top of that, GCash is considering an Initial Public Offering (IPO) in order to raise more capital for aggressive expansion.

With GCash being an avenue of growth for Globe, mobile data revenues improved, contributing to 45% of the parent company’s revenue in 2020.

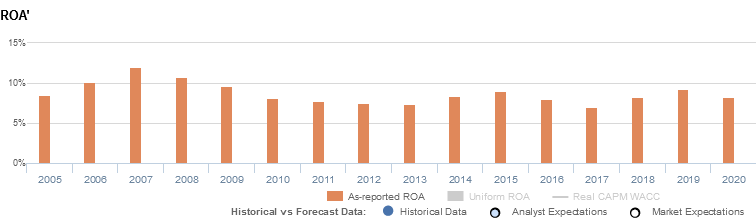

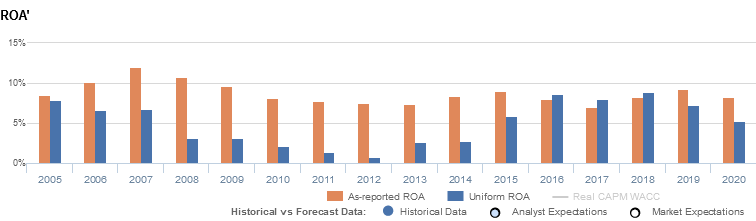

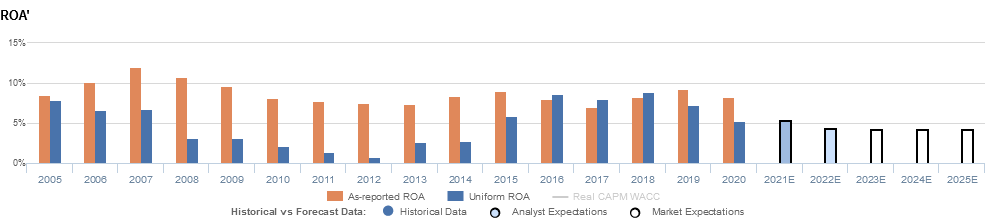

Looking at Globe’s as-reported profitability in 2020, it seems that its growth strategy with GCash has yet to pay off. The contributions from GCash were largely offset by revenue declines from other segments due to pandemic-related headwinds, with as-reported ROA slightly declining from 9% in 2019 to 8% in 2020.

In reality, Uniform ROA paints a worse picture, with Uniform ROA contracting from 7% to 5% in the same period, confirming that Globe’s strategy to enhance its mobile platform isn’t showing profits yet.

One of the main contributing factors to the misstatement of profitability is how Philippine Financial Reporting Standards (PFRS) accounts for property, plant, and equipment (PPE).

According to PFRS, PPE is recorded at historical costs – that is, in the purchasing power the year the fixed asset was recorded. But to better reflect reality, PPE should be adjusted for inflation.

In Uniform Accounting, adjustments have to be made so that the asset and cash flow values are reflecting the current purchasing power each year.

In 2020 alone, the company should have recognized PHP 82 billion more in fixed assets when adjusting for inflation.

When we add PHP 82 billion more to Globe’s PHP 340 billion asset base and with the many other adjustments Valens makes, we arrive at a TRUE earning power of 5%.

Globe’s earning power is weaker than you think in most years

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that Globe’s profitability is higher than what real economic metrics highlight in most years.

In reality, Globe’s true profitability has generally been weaker than its as-reported ROA except in 2016-2018.

As-reported ROA expanded from 9% in 2005 to 12% in 2007, before fading to cyclical levels from 2010-2020, while ranging from 7% to 9% and currently sitting at the middle of that range.

Meanwhile, after declining from 8% in 2005 to 1% in 2012, Uniform ROA rebounded to 8%-9% peaks in 2016-2018, before contracting to 5% in 2020.

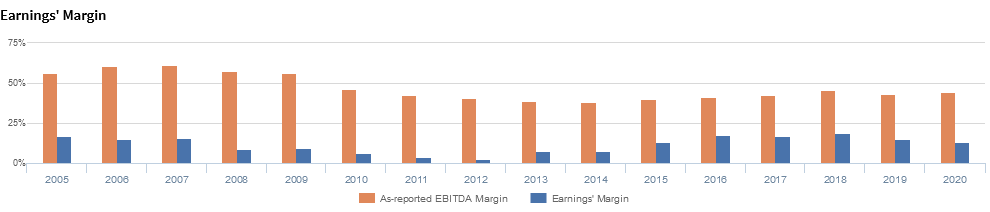

Globe’s earnings margin is much weaker than you think

Trends in Uniform ROA have been driven by trends in Uniform earnings margin, where Globe is substantially improving efforts in managing costs.

After shrinking from 17% in 2005 to 2% in 2012, Uniform margins recovered to a peak of 19% in 2018, and then dropped to 13% in 2020.

Looking at the firm’s margins alone, as-reported metrics make the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and Globe Telecom, Inc. Tearsheet

As our Uniform Accounting tearsheet for Globe Telecom (GLO:PHL) highlights, the company trades at a Uniform P/E of 21.5x, below the global corporate average of 23.7x but above its historical P/E of 19.6x.

Low P/Es require low EPS growth to sustain them. In the case of Globe, the company has recently shown a 25% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Globe’s sell-side analyst-driven forecast is to see Uniform earnings growth of 5% in 2021, before a 15% shrinkage in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Globe’s PHP 1,965.00 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 1% annually over the next three years. What sell-side analysts expect for Globe’s earnings growth is above what the current stock market valuation requires in 2021, but below the requirement in 2022.

Furthermore, the company’s earning power is below the long-run corporate average. Meanwhile, cash flows and cash on hand are below total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 120bps above the risk free rate. Together, this signals a high dividend and moderate credit risk.

To conclude, Globe’s Uniform earnings growth is in line with peers, and currently trades in line among average peer valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com