This internet service provider is easily connecting the country as it reaches a Uniform ROA of 19%, not 9%

Despite the challenges in the telecommunications industry, this company has managed to connect at least 50% of households in the Philippines. However, the as-reported metrics of the company do not appear to fully capture the company’s profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Dennis Anthony Uy is no stranger to the field of business and technology.

After finishing an Electronics Engineering course, he formed Jack’s Video – a Betamax rental shop in 1983, and ComClark Network and Technology Corp – an internet service provider in Clark Special Economic Zone in 1996.

As the company grew and new services were offered, Uy realized the challenges of the Philippines regarding internet speed.

One of the main factors why it’s difficult to provide fast internet for the country is the tedious process of building cell towers given the layers of bureaucracy one has to surpass. For instance, acquiring the required approved permit from 25 to 30 local government units (LGUs) usually takes around eight months just for one cell site.

Furthermore, the duopoly between Philippine Long Distance Telephone Company (TEL:PHL) and Globe Telecom (GLO:PHL) in the telecommunication industry became a challenge as their dominance effectively compromised innovation and internet quality.

Nevertheless, Uy saw an opportunity and used a micro-trenching process in order to utilize fiber optic cable lines, which were faster and more reliable than the usual copper-based digital subscriber line and cable internet.

In 2007, he and his wife, Ms. Maria Grace Y. Uy, started Converge ICT Solutions, Inc. (CNVRG:PHL) – the first pure end-to-end fiber internet network in the country.

After receiving the legal requirements to install and operate a telecommunications system in 2009 from congress as well as a nationwide broadband internet network in 2011 from the National Telecommunications Commission, the company commenced its fixed broadband internet operations in 2012.

In 2019, the company’s expansion plans to Visayas and Mindanao were boosted as Warburg Pincus, one of the world’s biggest private equity firms, invested $250 million in the company.

This helped the company cater to the surging demand for better internet services in 2020 as working from home became the standard amid the pandemic.

Converge’s goal is to reach over 15 million or 55% of Philippine households by 2025. As of June 30, 2022, its network has already reached 13.5 million or 52% of Philippine households.

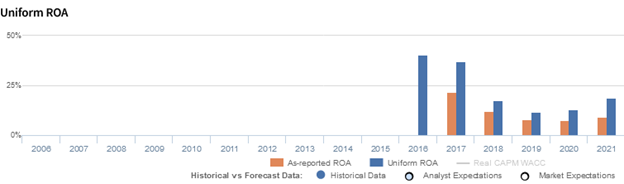

Overall, with Converge’s ability to offer premium products, we might expect it to be generating robust profitability. However, looking at as-reported metrics, it appears that these have only helped produce modest returns, with return on assets (ROAs) rebounding to 9% levels in 2021.

In reality, the company’s financial performance did better than presented, with Uniform ROAs performing 2x above at 19%.

One major contributing factor that has led to the misstatement of as-reported metrics is the failure to consider current liabilities in the profitability calculation.

Traditional ROA calculations for measuring a firm’s earning power only include current and long-term assets as part of the cost of investment.

However, a company’s ability to receive goods and services in advance of payments—the current operating liabilities—ought to be factored in as well.

Current liabilities (excluding short-term debt) are necessary for operations. Items such as accounts payable, accrued expenses, and others are used to maintain the firm’s current capital position. On the other hand, long-term liabilities are mostly just used to finance the business.

If a company has a ton of cash to service its current liabilities and we only factor in its cash, it would make the company look inefficient. In reality, the company is just being responsible for building liquid assets to meet short-term obligations.

As such, net working capital (current assets – current liabilities) is used for the firm’s ROA calculation. This shows a company’s real cash management ability and thereby, its true earning power.

When current liabilities are subtracted from Converge’s assets, along with the many other necessary adjustments made, this leads to a 19% Uniform ROA in 2021.

Converge’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that Converge’s profitability has been recently weaker than real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROAs have been understated over the past decade. For example, as-reported ROA was 9% in 2021, but its Uniform ROA was actually higher at 19%.

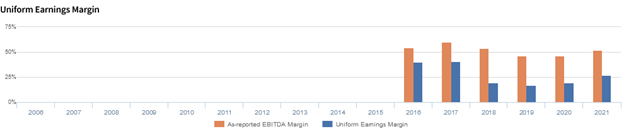

Converge’s earnings margins are less profitable than you think

Trends in Uniform ROA have been driven by trends in Uniform earnings margins. For more than two decades, as-reported metrics have overstated Converge’s earnings margin, a key driver of profitability.

Moreover, as-reported EBITDA margin has reached to 60%. In comparison, Uniform margins have yet to eclipse 41% over the same time period, making Converge appear to be a more profitable business than real economic metrics highlight.

SUMMARY and Converge ICT Solutions, Inc. Tearsheet

As our Uniform Accounting tearsheet for Converge ICT Solutions, Inc. (CNVRG:PHL) highlights, the company trades at a Uniform P/E of 12.6x, below the global corporate average of 18.9x, and its historical P/E of 16.5x.

Low P/Es require low EPS growth to sustain them. In the case of Converge, the company has recently shown a 155% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Converge’s sell-side analyst-driven forecast is to see Uniform earnings growth of 17% in 2022 and 25% in 2023.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Converge’s PHP 12.48 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 1% annually over the next three years. What sell-side analysts expect for Converge’s earnings growth is above what the current stock market valuation through 2023.

Moreover, the company’s earning power is 3x above the long-run corporate average. Moreover, cash flows and cash on hand are 3x above total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals moderate credit risk.

To conclude, Converge’s Uniform earnings growth is above its peer averages, but below its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com