This Philippine university gets an A for its digital foresight, achieving Uniform ROAs of 10%+

This university was able to develop its academic and online learning process through its technological initiatives years before the pandemic forced schools to adopt distance learning.

While its as-reported metrics do not show it, the company’s advantageous foresight on digital investments enabled it to achieve Uniform ROAs of more than 10%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In 2020, the Philippine education system faced one of its most difficult challenges to date—the COVID-19 pandemic.

The suspension of face-to-face classes forced schools to either resort to online classes or prematurely end the previous academic year.

On top of that, schools had to follow the strictly-implemented IATF (Inter-Agency Task Force for the Management of Emerging Infectious Diseases) guidelines, allowing only 50% of staff to retain on-site work in their respective campuses.

Until now, the country hasn’t fully opened its educational institutions to in-person classes due to the continued rise of COVID-19 infections, hindering around 27 million students from receiving better-quality education.

Luckily, the Far Eastern University, Incorporated (FEU:PHL) was way ahead of this issue—investing heavily in IT infrastructure and systems as well as education technology—even before the pandemic started.

Specifically, in 2015, the school had already adopted the Canvas Learning Management System (LMS), an online portal also used by Harvard University, to administer efficient digital learning for both students and teachers.

Under this approach, students were offered three flexible modes of learning:

- Mixed Online Learning (MOL) – wherein student-teacher engagement is required most of the time

- Asynchronous Online Learning (AOL) – wherein students can get learning materials from Canvas

- Total Analogue Learning (TAL) – wherein students can get learning materials through a USB harddrive

Besides these learning-related developments, FEU has also focused on securing digital enhancements for its business processes, which helped the school execute seamless enrollment and administrative tasks.

Pursuing digital learning enhancements and initiatives has even helped FEU achieve a 3% increase in educational income despite the 10% drop in enrollment.

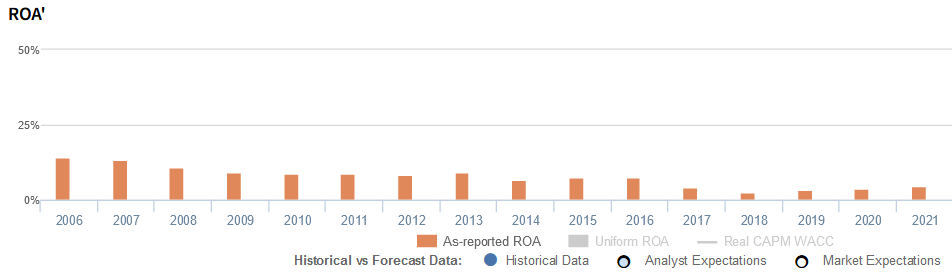

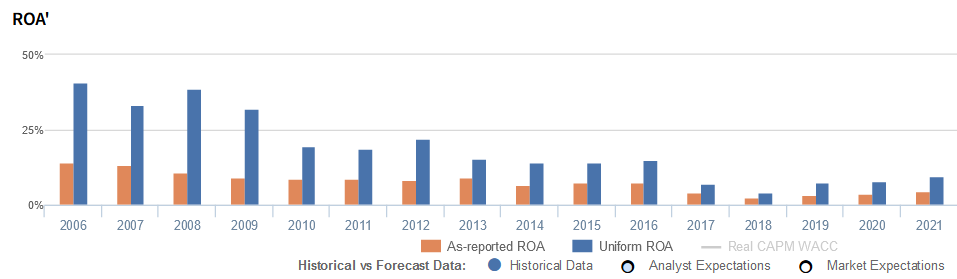

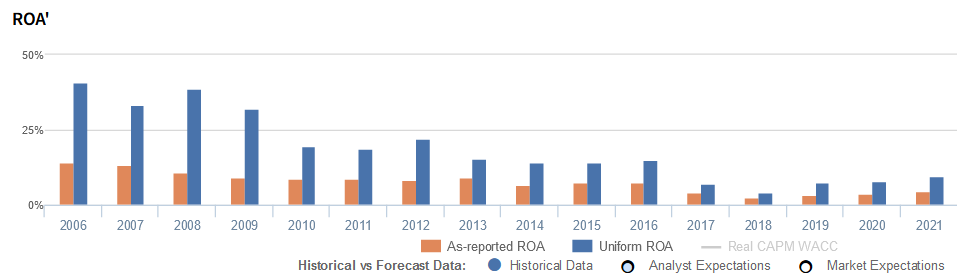

Overall, FEU looks poised to survive and thrive despite industry challenges during the pandemic. However, looking at as-reported metrics, it looks like the school hasn’t been profitable these past five years, with return on assets (ROAs) only reaching below cost-of-capital levels.

In reality, thanks to the company’s advantageous foresight on digital investments, it has been able to achieve higher ROAs than as-reported, with Uniform ROAs reaching 10% in recent years.

One of the main contributors to such discrepancy is its treatment of excess cash. While as-reported financials treat FEU’s entire cash balance as part of its asset base, Uniform Accounting removes the cash that’s not necessary to operate and fulfill obligations—cash above what one might view as “operating” cash.

The purpose of removing excess cash is to see what the true operating assets of the firm are. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

In 2021 particularly, FEU has PHP 2.9 billion worth of excess cash, making up 19% of the company’s as-reported assets.

Removing excess cash and applying the other adjustments Valens makes, FEU’s 4% as-reported ROA and PHP 15.4 billion asset base are adjusted to reveal its TRUE Uniform ROA of 10%, by essentially utilizing just PHP 9.8 billion of Uniform assets.

FEU’s profitability is stronger than you think in recent years

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics reveal.

For example, Uniform ROA for FEU was 10% in 2021, substantially higher than the as-reported ROA of 4%, making the company appear to be a much weaker business than real economic metrics highlight for the past sixteen years.

Moreover, since 2011, Uniform ROA gradually declined from a high of 41% in 2006 to a low of 4% in 2018, before rebounding to 10% in 2021. Meanwhile, as-reported ROA has contracted from a high of 14% in 2005 to 3%-4% levels in 2017-2021.

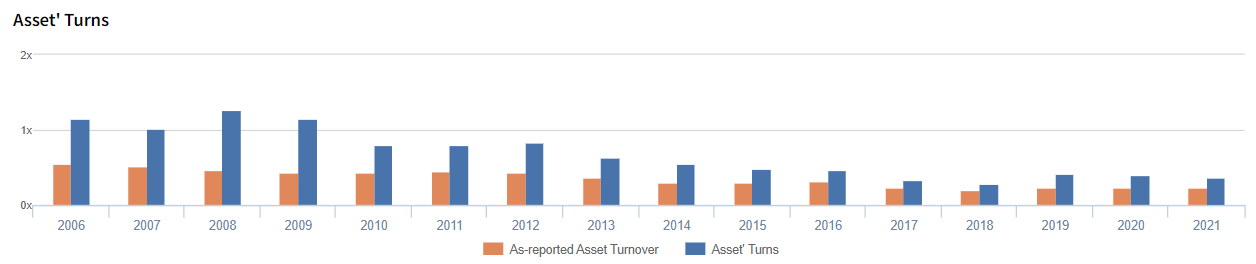

FEU’s historical asset turns are stronger than you think

Strength and overall declines in FEU’s Uniform ROA have been driven primarily by trends in Uniform asset turns. In fact, Uniform turns have been higher than as-reported asset turnover in each of the past sixteen years.

Since 2005, as-reported asset turnover has slowly contracted from 0.5x highs in 2005-2008 to 0.2x lows in 2017-2021.

Meanwhile, Uniform turns gradually fell from 1.3x in 2008 to 0.3x-0.4x levels in 2017-2021.

Looking at the firm’s turns alone, the as-reported metrics are making the firm appear to be a less asset efficient business than is accurate.

SUMMARY and The Far Eastern University, Incorporated Tearsheet

As our Uniform Accounting tearsheet for The Far Eastern University, Incorporated (FEU:PHL) highlights, the company trades at a Uniform P/E of 15.9x, which is below the global corporate average of 24.0x, but around its historical P/E of 18.1x.

Low P/Es require low EPS growth to sustain them. In the case of FEU, the company has recently shown a 69% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, FEU’s sell-side analyst-driven forecast is to see an 11% and immaterial Uniform earnings decline in 2022 and 2023, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify FEU’s PHP 535.00 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 5% over the next three years. What sell-side analysts expect for FEU’s earnings growth is below what the current stock market valuation requires in 2022, but above its requirement in 2023.

However, the company’s earning power is 2x the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low dividend risk.

To conclude, FEU’s Uniform earnings growth is above its peer averages, but it currently trades in line with its average peer valuations.

About the Philippine Markets Newsletter

|“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!,br>

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com