This retail giant is building more big-box stores to up its one-stop shop game. With a 35.9x Uniform P/E, the market is pricing that in.

As the 20th richest Filipino according to Forbes, William Belo owns the company that dominates the Philippine home improvement space.

With 40 years of experience and 36 big-box stores, he took his company public in 2017. With the additional funds, the company was able to build 21 more stores nationwide.

As-reported financials suggest that its post-IPO results have been no different than pre-IPO.

But TRUE UAFRS-adjusted (Uniform) metrics is revealing its potential to be The Home Depot, Inc. (not Lowe’s) of the Philippines, which the market is starting to price in.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The boom in the real estate market in the Philippines since 2004 has helped the home improvement industry recover from the slump brought by the 1997 Asian financial crisis.

Every year, more and more building permits are being approved, increasing the available housing supply. Since 2007, the number of annually approved residential building permits has risen 82%.

A lot have taken this opportunity to invest in residential property, to be rented out or flipped at a higher price.

The emergence of different sources of financing from Pag-IBIG, the bank, or in-house has made owning or investing a home a more attainable goal for Filipinos today.

In addition, the number of people in the age group of 25-34 who are looking to buy or rent a house has gone up, now making up almost half of all online property searches.

Given the high prices of real estate in the city, more and more buyers in the 25-34 age range are expanding their search outside of Metro Manila towards the provinces of Cavite, Laguna, and Rizal.

In addition, residential house developers often turn over the houses to the new owner bare-type finished because it is cheaper. It also gives buyers the opportunity to be creative and style their own homes based on their preferred lighting, tiles settings, home interior, plumbing, and many more.

This rising trend is popularizing the concept of the depot, where people can conveniently buy all their home construction needs from one shop and find the perfect design that will match their taste.

Wilcon Depot’s “one-stop shop” offers its consumers multiple choices in every product category. Customers can choose whether to buy home improvement needs from local or imported product lines, based on the latest style of home.

As the leading home improvement supplier in the Philippines, Wilcon maintains its efficiency by having well-trained and knowledgeable personnel. Each of its sales personnel has a portable tablet linked to an electronic inventory system, that enables them to quickly check available products in all of their branches.

Ever since the company’s humble beginning in 1977 as a 60-square meter hardware shop, it has carried a wide range of the latest building and finishing materials from both local and international markets.

26 years later, Wilcon launched its first big-box store with a complete selection of products and services that provide reliable delivery and knowledgeable sales personnel.

The company envisioned to offer its customers with top grade quality products as well as customer satisfaction by providing convenient shopping in air conditioned and mall-based shops.

In 2009, Wilcon established a mall-based format shop for their Home Essentials retail store. This store offers its customers home must-haves in an organized section, making it easy to browse through available options, especially for the DIYers.

Wilcon continued its expansion by opening additional stores outside Metro Manila, with store sizes ranging from 2,800 sqm to 31,000 sqm, a far cry from its original 60 sqm.

The expansion targets customers in the niche market in the home building and construction industry.

In addition to the company’s continuous expansion, Wilcon launched its digital store in early 2019.

Thanks to the company’s effective growth strategy over the years, Wilcon has become a retail giant, enjoying half of the market share in the country, now with a total of 57 operating stores nationwide.

Wilcon had over 40 years experience in the industry before it went public in 2017. Since its IPO, its stock price has been on an upward trend, increasing by 350%+ from PHP 5.05 to PHP 18.10.

Uniform metrics are reflecting the same growth potential that the market is starting to see, which as-reported financials have failed to do.

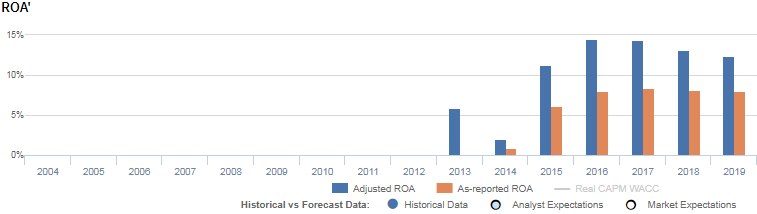

Its recently released 2019 financials are reporting 8% return on assets (ROA), but after removing non-essential assets, Wilcon’s TRUE earning power is actually 12%.

One such non-essential asset is excess cash.

Large amounts of cash, in the bank and in the form of treasury bonds, can overstate a company’s assets. While it is integral for a business to operate and satisfy liquidity, cash that is more than required is just sitting in the balance sheet, offering little or no return and diluting ROA.

By subtracting this excess cash from the balance sheet (in asset and equity) and with many more adjustments Valens makes, we get to see a clearer picture of what Wilcon is building.

Wilcon’s earning power is actually more robust than you think

As-reported metrics significantly understate Wilcon’s (WLCON:PHL) profitability. For example, Uniform ROA for Wilcon was 12% in 2019, greater than Uniform ROA of 8% by half, making the company appear to be a much weaker business than real economic metrics highlight.

Moreover, as-reported ROA has stagnated around 8% levels since 2016, a year before its IPO. Meanwhile, Uniform ROA was at all-time highs at 15% in 2016, before slowly falling to 12% in 2019.

Trends in Uniform ROA have been driven by growth in assets outpacing growth in earnings. Also, Uniform asset growth has been almost greater than as-reported, especially when excluding 16% shrinkage in 2014.

The company’s financials have been understating the expansion of their true asset base, which is mostly made up of their stores.

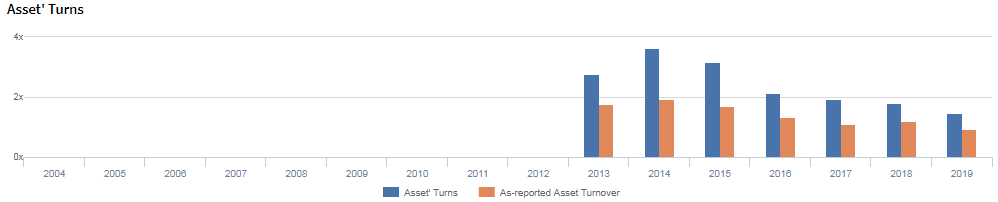

Wilcon’s asset turns are stronger than you think

Wilcon’s Uniform asset turns have trended downwards, but not to the degree that as-reported metrics state. This implies that the company is generating better sales per peso spent in assets.

Historically, Uniform asset turns reached a high of 3.6x in 2014, before falling to 1.5x in 2019. Similarly, as-reported asset turns peaked at 1.9x in 2014, before dropping to 0.9x in 2019.

Due to as-reported asset turns being far lower than its Uniform counterpart every year since, it has significantly distorted the market’s perception of the firm’s profitability levels.

At current valuations, markets are pricing in expectations for stability in Uniform asset turns.

SUMMARY and Wilcon Depot Tearsheet

As our Uniform Accounting tearsheet for Wilcon highlights, Uniform P/E trades at 35.9x, which is above market average and historical average levels.

High P/Es require high EPS growth to sustain them. In the case of Wilcon, the company has recently shown 37% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Wilcon’s sell-side analyst-driven forecast is for Uniform earnings to grow by 12% in 2020, before a more robust growth of 20% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP18 per share. These are often referred to as market embedded expectations.

To meet the current market valuation levels of Wilcon, the company would need to grow 19% of Uniform earnings each year over the next three years.

What sell-side analysts expect for Wilcon’s earnings growth is in line with what the current stock market valuation requires in 2019.

The company’s earning power is 2x the corporate average, and the company has low dividend risk, signaling that their cash flow risk to the company’s operations and credit profile in the future is low.

To conclude, Wilcon’s Uniform earnings growth is around peer averages in 2019 and the company is trading above peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com