This universal bank’s UITF invests in companies with an earning power almost 2x its as-reported metrics based on Uniform Accounting!

This six-year unit investment trust fund (UITF) has been underperforming its benchmark, the Philippine Stock Exchange Index (PSEi).

However, the UITF’s year to date performance is neck-and-neck with the PSEi, with the fund and its benchmark down 25% and 24%, respectively.

As-reported metrics would leave investors confused with the fund’s stock picks. However, Uniform Accounting financial metrics show that this fund has an earning power almost 2x as-reported levels.

In addition to examining the fund’s portfolio, we are including fundamental analysis of one of the fund’s largest holdings, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Philippine Markets Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

We’ve written about one of United Coconut Planters Bank‘s (UCPB) UITFs before—the UCPB Equity Fund.

UCPB was established in 1963, and is the first private Philippine bank to become a universal bank in 1981. Today, it caters to its highly-diversified customers by delivering a wide-range of banking services in consumer finance, commercial credit, and corporate and investment banking, among others.

This week, we’re focusing on another UITF they offer, the UCPB High Dividend Fund (UHDF).

UHDF’s investment strategy is to generate long-term capital appreciation and steady income streams by investing in domestic, listed common and preferred shares.

However, the PSEi, the fund’s benchmark, has been outperforming the UITF since its inception on April 8, 2014.

UHDF rose from a net asset per value (NAVPU) of PHP 1.00 in its inception to a record PHP 1.15 in April 2015, delivering a 15% investment growth.

After reaching its peak, UHDF’s NAVPU slowly descended before falling to PHP 0.99 in August 2015 due to the flash crash. This resulted in strong selling that week, with the influx of sell orders against fewer bids pushing stock prices even lower. Overall, the fund and its benchmark fell 14% and 16% over that time period, respectively.

UHDF’s NAVPU rebounded to PHP 1.06 in October 2015, before once again dropping to PHP 0.94 in January 2016 due to the oil price crash. Its 11% decline, albeit a loss, outperformed PSEi’s 17% decline over that time span.

After ending 2019 with a NAVPU of PHP 1.07, the fund plunged to a historical low of PHP 0.71 in March 2020 due to the coronavirus-induced market downturn. It has since settled at PHP 0.80 as of August 24, 2020. Year to date, both the fund and the PSEi are down by 25% and 24%, respectively.

Looking at UHDF’s investments using as-reported metrics, it is not apparent that the fund invests in stable and established companies.

As-reported metrics would have investors believe that this portfolio consists of companies that do not generate economic profit. However, Uniform Accounting reveals the truth behind the companies this fund invests in.

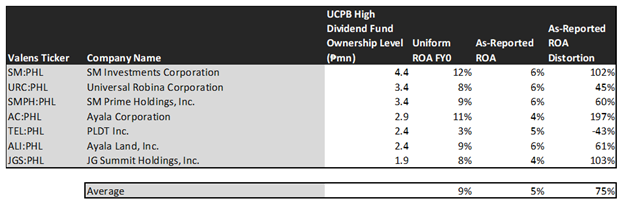

The table below shows the core non-financial holdings of the UHDF along with their Uniform return on assets (ROA), as-reported ROA, and ROA distortion—the difference between Uniform and as-reported ROA.

All companies in the UCPB High Dividend Fund show as-reported ROAs that range around and below global cost-of-capital levels, suggesting that they are not generating economic profit. In 2019, the fund generated an average as-reported ROA of 5%, below the global corporate average returns of 6%.

However, on a Uniform Accounting basis, this UITF has actually delivered stronger earnings with an average Uniform ROA of 9%, almost 2x as-reported levels. Most of its companies have strong returns, with Uniform ROA above 6% global average returns.

The Uniform Accounting framework addresses financial statement inconsistencies attributable to the flaws present in the Philippine Financial Reporting Standards (PFRS). This enables investors to determine the true underlying performance of companies and avoid distorted financial analysis and valuation.

As such, it should not be surprising that when analyzing the non-financial holdings of the fund, the figures that easily stand out are the large discrepancies between Uniform ROA and as-reported ROA for these companies.

While at a glance, the difference between as-reported ROA and Uniform ROA may not seem that great, the distortion in percentage ranges from -43% to 197%, with Ayala Corporation (AC:PHL), JG Summit Holdings, Inc. (JGS:PHL), and SM Investments Corporation (SM:PHL) all having distortions above a hundred percent.

As-reported ROA understates the profitability of AC, suggesting a below average company with an as-reported ROA of 4%. In reality, this leading conglomerate is a high-quality firm with an 11% Uniform ROA, almost thrice the as-reported number. Over the past decade, AC has never seen its Uniform ROA dip below 10%.

Similarly, JGS is not just a 4% ROA firm like what as-reported numbers suggest. It is, in fact, an above-average company with an 8% Uniform ROA, consistently generating returns above 7% over the past five years.

By focusing on as-reported metrics alone, UCPB would never pick most of these companies because they look like anything but profitable businesses.

That said, looking at profitability alone is insufficient to deliver superior investment returns. Investors should also identify if the market is significantly undervaluing the company’s earnings growth potential.

This table shows the earnings growth expectations for the major non-financial holdings of the fund. It features three key data points:

- The 2-year Uniform earnings per share (EPS) growth represents the Uniform earnings growth the company is likely to have for the next two years. The earnings number used is the value of when we convert consensus sell-side analyst estimates to the Uniform Accounting framework.

- The market expected Uniform EPS growth represents what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next two years to justify the current stock price of the company. This is the market’s embedded expectations for Uniform earnings growth.

- The Uniform EPS growth spread is the difference between the 2-year Uniform EPS growth and market expected Uniform EPS growth.

On average, Philippine companies are expected to have 6% annual Uniform earnings growth over the next two years. However, UHDF’s major holdings are forecast to underperform with a 5% projected Uniform earnings decline in the next two years, while the market is seeing a 1% Uniform EPS decline.

Among these companies, only PLDT, Inc. (TEL:PHL) and SM have positive Uniform earnings growth dislocation.

The market is pricing TEL’s Uniform Earnings to grow only by 5% in the next two years. However, sell-side analysts are projecting the company’s earnings to accelerate by 41% moving forward.

Meanwhile, the market is expecting SM’s Uniform earnings to plummet by 11%, while analysts are projecting lower earnings shrinkage of 8% for the company in the next two years.

Overall, as-reported numbers would have investors incorrectly conclude that this portfolio consists of low-quality companies. While these firms suffer from the adverse effects of the coronavirus pandemic, dragging down their short-term earnings growth expectations, Uniform Accounting metrics show that these companies are high quality with intact business models that would drive economic profitability moving forward.

SUMMARY and Universal Robina Corporation Tearsheet

Today, we’re highlighting one of the largest individual stock holdings in the UCPB High Dividend Fund—Universal Robina Corporation (URC:PHL).

As the Uniform Accounting tearsheet for URC highlights, it trades at a Uniform P/E of 32.9x, well above the global corporate average P/E of 24.3x, but around its historical average of 34.5x.

High P/Es require high EPS growth to sustain them. In the case of URC, the company has recently shown a robust 23% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that poorly track reality. However, sell-side analysts have a strong grasp on near-term financial forecasts like revenue and earnings.

We take sell-side forecasts for PFRS earnings as a starting point for our Uniform earnings forecasts. When we do this, URC’s sell-side analyst-driven forecast shows that Uniform earnings is expected to decline by 11% in 2020, before accelerating by 12% in 2021.

Based on the current stock market valuations, we can back into the required earnings growth rate that would justify PHP 137.20 per share. These are often referred to as market embedded expectations.

Uniform earnings would have to grow by 9% over the next three years to justify current price levels. What sell-side analysts expect for URC’s earnings growth is below what the current stock market valuation requires in 2020, but above what the market requires in 2021.

The company has an earning power that has consistently been well above global long-run corporate averages—based on its Uniform ROA calculation. Since the combination of the company’s cash flows and cash on hand are at 181% of total obligations, URC has a low dividend risk.

To conclude, URC’s Uniform earnings growth is below peer averages. Moreover, the company is trading well above peer average valuations.

About the Philippine Market Daily

“Friday Uniform Portfolio Analytics”

Investors who don’t engage in the buying or selling of securities for a living oftentimes rely on professionals to manage their own investments within the scope of their investment policies.

With so many funds and managers out there, it can get confusing and difficult to decide which one best suits your needs as an investor.

Every Friday, we focus on one fund in the Philippines and take a deeper look into their current holdings. Using Uniform Accounting, we identify the high-quality stocks in their portfolio which may not be obvious using the as-reported numbers.

We also identify which holdings may be problematic for the fund’s returns that they would need to reconsider from a UAFRS perspective.

To wrap up the fund analysis, we highlight one of their largest holdings and focus on key metrics to watch out for, accessible in our tearsheets.

Hope you’ve found this week’s focus on UCPB High Dividend Fund interesting and insightful.

Stay tuned for next week’s Friday Uniform Portfolio Analytics!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com