Uniform Accounting has processed and disinfected this company’s distortions with a Uniform ROA of 5%, not 7%

This company is an example of how even having a near-monopoly in a niche market does not always translate to great profitability. Although its as-reported data show higher returns in recent years, its Uniform ROA actually tells a different story to investors.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Founded in 1934 as the Mabuhay Rubber Corporation, this company was initially a shoemaker.

Through the years, the company would diversify its operations into Poly Vinyl Chloride (PVC) resin, which would soon be its main product line. In order to align its identity with the main product, the company renamed itself as the Mabuhay Vinyl Corporation (MVC:PHL) in 1966.

Soon after publicly listing in 1997, Mabuhay Vinyl shifted its main product line once again and focused on its chlor-alkali business after the Asian economic crisis.

Chlor-alkali is a process that is used to chemically produce chlorine and caustic soda. Chlorine is commonly used as a disinfectant for drinking water and swimming pools as well as bleach for household cleaning.

Meanwhile, caustic soda or commonly referred to as lye has been found in substances such as soap, detergent, paper production, and even local desserts in kutsinta and pichi-pichi.

As of today, Mabuhay Vinyl is the sole local producer of chlor-alkali. Risks of losing market share are minimal as competition for commercially-used chlorine and caustic soda mainly comes from traders and importers.

In addition, Mabuhay Vinyl is the largest importer of liquid caustic soda in the country, indicating robust demand for their product that is beyond their current capabilities.

In order to meet growing demand, the company plans to expand the production capacity of its Iligan Plant by 68%. Through capacity expansion and upgrading its facilities, this project emphasizes the company’s focus on growth and cost-efficiency.

Going forward, one of the major risks that Mabuhay Vinyl looks out for is the movement in liquid caustic prices in the foreign markets.

Although sales volume in 2021 increased from 2020, so did the company’s costs of production, importation, and distribution, which resulted in lower margins.

Additionally, with inflationary pressures improving, a sustainable rise in liquid caustic prices could negatively pressure the company’s profitability.

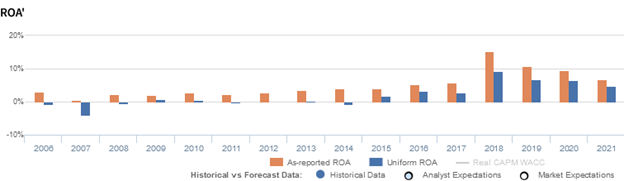

Looking at as-reported metrics, it appears that Mabuhay Vinyl is generating shareholder value, with return on assets (ROAs) reaching above cost of capital levels since 2018.

In reality, the company’s performance actually did worse than presented, with recent Uniform ROAs of 5%-6%, which are levels that are only in-line with its cost of capital.

The distortion in Mabuhay Vinyl’s ROA mainly comes from PFRS allowing the firm to extend the lives of its fixed assets, which allows the company’s old assets to still be in use.

Extending an asset’s life isn’t inherently an issue, but keeping its book value does. Without adjusting for inflation, a company looks more efficient than in reality when tying present-day cash flows to assets purchased years or decades ago.

In 2021, Mabuhay Vinyl’s total as-reported assets amounted to PHP 3.5 billion, but the company should be recognizing PHP 1.6 billion or 45% more in assets when adjusting its PP&E for inflation.

Applying the inflation adjustment, along with many other necessary adjustments, leads to a 5% Uniform ROA in 2021, significantly lower than the as-reported ROA of 7%.

Mabuhay Vinyl’s earning power is weaker than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that Mabuhay Vinyl’s profitability has been stronger than real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROAs have been overstated over the past decade. For example, as-reported ROA was 7% in 2021, but its Uniform ROA was actually lower at 5%.

Mabuhay Vinyl’s margins are weaker than you think

As-reported metrics significantly overstate Megaworld Corporation’s profitability trends. For example, as-reported EBITDA margin for the company was 21% in 2021, higher than Uniform earnings margin of 10%, making the firm appear to be a much stronger business than real economic metrics highlight

Moreover, as-reported asset turnover has reached up to 26%. In comparison, Uniform earnings margins have yet to peak beyond 13% in the same time period, distorting the market’s perception of the company’s historical profitability trends.

SUMMARY and Mabuhay Vinyl Corporation Tearsheet

As our Uniform Accounting tearsheet for Mabuhay Vinyl Corporation (MVC:PHL) highlights, the company trades at a Uniform P/E of 12.0x, below the global corporate average of 20.6x, but above its historical P/E of 10.0x.

Low P/Es require low EPS growth to sustain them. In the case of Mabuhay Vinyl, the company has recently shown a 20% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Mabuhay Vinyl’s sell-side analyst-driven forecast is to see Uniform earnings shrink by 1% through 2023.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Mabuhay Vinyl’s PHP 5.39 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 10% annually over the next three years. What sell-side analysts expect for Mabuhay Vinyl’s earnings growth is above what the current stock market valuation requires through 2023.

However, the company’s earning power is below the long-run corporate average. Yet, cash flows and cash on hand are nearly 5x above total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

Lastly, Mabuhay Vinyl’s Uniform earnings growth is well below its peer averages, but in line with its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com