Uniform Accounting shows how this company’s marketing efforts are leading to Uniform returns above global corporate averages

Building a strong brand is essential for businesses in the consumer goods industry to thrive. One way to attain that is through effective brand awareness marketing.

This snack food and beverage company owns many of the famous brands that Filipinos have been enjoying since childhood. Through its marketing initiatives, the company has grown to become a key player in the markets it operates.

The as-reported metrics suggest that the firm’s recent performance has barely been sufficient in generating economic value, but the Uniform data shows its brands to be more valuable than perceived.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Brand awareness is all about creating consumer connection. It familiarizes consumers about the product and shows them how different the product is from other offerings in the market.

Many consumer good companies have been heavily reliant on brand awareness. Take the soda beverage market for example: Coca-Cola (KO) was able to rebrand its product as a refreshing beverage when it was previously known as a medicine.

Our Philippine Markets Daily article on Coca-Cola discussed how the firm was able to rebrand through a series of marketing strategies. Its campaigns centered on creating an emotional impact on consumers, building great consumer connection.

One of the Philippines’ largest snack food and beverage companies has also been using effective brand awareness marketing to dominate in many consumer goods segments.

Universal Robina Corporation (URC:PHL) leads the snack food market with its Piattos and Nova chips, Cloud9 and Hello! chocolate bars, and many other well-known brands. The firm also controls the ready-to-drink tea market with its C2 brand, and is one of the largest producers of instant coffee.

With a brand portfolio too extensive to enumerate, URC has been heavily reliant on brand awareness marketing. Compared to its public peers, URC dedicates the largest proportion of revenues to marketing expenses.

Whenever the firm launches a new product, it is often accompanied by promotions and advertisements to immediately generate strong product recognition. Thereafter, the company runs continuous advertisements to retain consumer interest.

URC has been pretty consistent in employing continuous advertisements, in particular with its potato chip brand Piattos. Among all their potato chip products, Piattos has received the most frequent advertising exposure, with a new marketing campaign launched every two years since 2009.

Another URC brand that has received intense marketing over the years is C2. Its product launch in 2004 was so successful that it quickly became the most profitable URC brand in just over a year after launch.

To this day, the company has been able to maintain strong consumer demand for C2 because of its endless marketing campaigns, with a massive 84.4% market share in ready-to-drink teas as of Q2 2020.

URC’s efforts to continuously market their products have allowed the firm to dominate in multiple food and beverage categories. For this reason, the firm has been able to post Uniform returns above the 6% global corporate average for almost a decade.

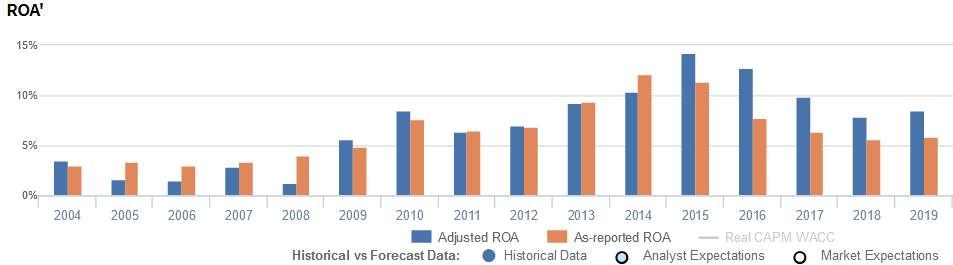

However, URC has seen returns decline as the firm expanded its global operations. Following the PHP 8.2 billion acquisition of Griffin’s Foods in 2015, the firm’s Uniform ROA fell from a peak of 14% in 2015 to 9% in 2019.

As-reported metrics are claiming the company’s downfall to be much more severe, with as-reported ROA falling from 11% in 2015 to just 6% in 2019.

The growing deviation of the as-reported metrics from the company’s true performance stems from the treatment of goodwill. With the 2014 Griffin’s Foods acquisition, the firm’s goodwill ballooned from PHP 0.8 billion to PHP 14.7 billion.

Goodwill is a purely accounting-based item and does not actually represent any asset URC uses for its operations. As a result, URC’s true asset base has been materially overstated and is downplaying its marketing-led performance.

Removing goodwill along with the other necessary adjustments in Uniform Accounting, Universal Robina Corporation should be recognizing PHP 36 billion less in assets and a 9% Uniform ROA.

URC’s recent earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

URC’s Uniform ROA has actually been higher than its as-reported ROA for the past five years. For example, as-reported ROA was 6% in 2019, but Uniform ROA is displaying stronger profitability at 9%.

Through Uniform Accounting, we can see that the company is still generating true ROAs above the 6% global corporate average.

As-reported ROA maintained 3% levels from 2004-2007, before improving to 8% in 2010 and subsequently contracting to 7% levels in 2011-2012. Thereafter, as-reported ROA rose to a peak of 12% in 2014, before regressing to 6% levels from 2017-2019.

Meanwhile, after fading from 4% in 2004 to a low of 1% in 2008, Uniform ROA jumped 9% in 2010, but compressed to 6% in 2011. Then, Uniform ROA expanded to a peak of 14% in 2015, before falling to just 9% in 2019.

URC’s recent asset utilization is more efficient than you think

URC’s recent performance has been driven primarily by stronger Uniform asset turns, a key driver of profitability.

From 2004-2007, as-reported asset turnover remained at 0.6x levels, before expanding to 1.2x peaks in 2013-2014 and subsequently fading to 0.8x levels in 2016-2019. Meanwhile, after sustaining 0.7x-0.8x levels from 2004-2008, Uniform turns soared to 1.2x highs in 2015-2016, before contracting to 1.0x in 2019.

As-reported metrics are making the firm appear to be a less asset efficient business than real economic metrics highlight.

SUMMARY and Universal Robina Corporation Tearsheet

As the Uniform Accounting tearsheet for URC highlights, the Uniform P/E trades at 32.8x, which is above corporate average valuation levels but around its own history.

High P/Es require high EPS growth to sustain them. In the case of URC, the company has recently shown a 23% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, URC’s sell-side analyst-driven forecast calls for a 6% Uniform EPS decline in 2020 and an 11% Uniform EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify URC’s PHP 142.90 stock price. These are often referred to as market embedded expectations.

The company would need to grow its EPS by 10% each year over the next three years to justify current valuations. What sell-side analysts expect for URC’s earnings growth is below what the current stock market valuation requires.

Furthermore, the company’s earning power is above the long-run corporate average. Meanwhile, cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, URC’s Uniform earnings growth is below peer averages, but the company is trading well above its peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com