With a solid foundation, this company is building its way back up better by constructing a Uniform ROA of 5%, not 1%

Amid its legal headwinds, this construction company is building back its profitability towards pre-pandemic levels with newly awarded projects. While historical as-reported data show an unprofitable environment based on the company’s strategies, its Uniform ROA actually says otherwise.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

With a PHP 5 trillion budget in 2022—the country’s largest government budget plan ever—the Philippine government aims to stimulate economic growth and recover from the impact of COVID-19. Included in that budget is PHP 1 trillion for infrastructure spending to continue its Build, Build, Build program and support for state corporations and local government units.

One of the largest infrastructure conglomerates in the country, Megawide is set to benefit from this as the company shifts its focus towards the government’s infrastructure development plans.

In 2004, Megawide Construction Corporation (MWIDE:PHL) was incorporated as a construction company. It set itself apart from its peers through its adoption of European construction systems and techniques, making it the most advanced formwork system in the country.

With its ability to reduce construction time and allow for quicker project turnover, Megawide attracted newly awarded projects such as the first landport of the Philippines in the Parañaque Integrated Terminal Exchange (PITx) project.

Furthermore, the company was able to ramp up projects in 2021 like the Department of Transportation’s Malolos Clark Railway Phase 1 project. In private infrastructure projects, Megawide continued construction work for Suntrust Home Developers’ Suncity West Side City project and Megaworld’s Newport Link project.

These major projects position Megawide’s construction segment as the company’s primary growth driver to return to profitability.

However, in November 2021, Megawide faced legal problems as the Lapu-Lapu City Regional Trial Court issued arrest warrants against foreign nationals and Filipino executives from GMR Megawide Cebu Airport Corp. (GMCAC), a joint venture between India’s infrastructure giant GMR Group and Megawide, for allegedly violating the Anti-Dummy Law.

According to the court’s evidence, foreigners were authorized to manage and operate over Mactan-Cebu International airport (MCIA), a Philippine public utility, with the awareness and approval of Filipino executives.

This negative publicity against the company may discourage new contracts from being awarded to Megawide going forward. With almost 84% of its revenue coming from the construction segment in 2020, this may become a headwind for growth.

In 2020, most of the company’s operations resumed late in the year as the government eased quarantine restrictions, allowing construction and landport segments to buffer revenue declines.

Still, total revenues declined as operations like its airport segment struggled with the unpredictable domestic and international travel bans amidst the pandemic.

Looking at the as-reported metrics, the company continued to produce returns below cost-of-capital levels, implying that the company has generated little to no economic value for its stockholders since 2008.

In reality, the company’s real economic profitability significantly has actually been more robust, and well above than as-reported metrics show.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of capitalized computer software licenses on Megawide’s balance sheet.

In 2020, computer software licenses sit at nearly PHP 30 billion, which is about 37% of the company’s total assets, arising from costs incurred to acquire and install the specific software.

Capitalized computer software license is an intangible asset that is unrepresentative of Megawide’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Megawide’s earning power. Removing intangible assets and other adjustments, we can see that the company isn’t producing paltry returns. In fact, it has been the opposite, with the company earning robust returns that have been 5x greater.

Megawide’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that the company is weaker than what real economic metrics highlight.

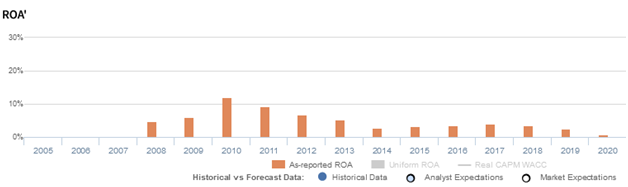

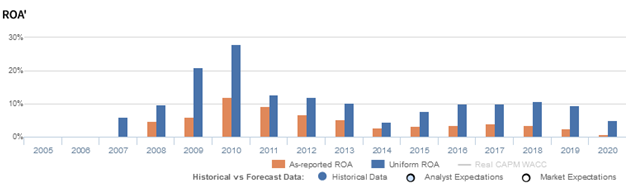

Megawide’s Uniform ROA has actually been higher than its as-reported ROA in the past thirteen years. For example, as-reported ROA was 1% in 2020, but its Uniform ROA was actually near cost-of-capital levels at 5%.

Specifically, as-reported ROA improved from 5% in 2008 to a high of 12% in 2010, before slowly fading to 1% in 2020.

Meanwhile, after expanding from 6% in 2007 to a peak of 28% in 2010, Uniform ROA fell to 5% in 2014. Thereafter, Uniform ROA recovered to 10% levels in 2016-2017, before compressing to 5% in 2020.

Megawide’s asset turns are stronger than you think

Strength in Megawide’s Uniform ROA has been driven by strength in its Uniform asset turns. Uniform turns have been higher than as-reported asset turnover in each of the past fourteen years.

From 2007-2010, as-reported asset turnover improved from 0.9x to 1.4x, before slowly eroding to 0.2x in 2018-2020. Meanwhile, Uniform turns rose from 1.6x in 2007 to 3.9x in 2010, before gradually compressing to 0.4x in 2020.

Looking at the firm’s turns alone, the as-reported metrics are making the firm appear to be a less asset efficient business than is accurate.

SUMMARY and Megawide Construction Corporation Tearsheet

As our Uniform Accounting tearsheet for Megawide Construction Corporation (MWIDE:PHL) highlights, the company trades at a Uniform P/E of 18.8x, below the global corporate average of 24.0x and its historical P/E of 38.4x.

Low P/Es require low EPS growth to sustain them. In the case of Megawide, the company has recently shown a 161% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Megawide’s sell-side analyst-driven forecast is to see Uniform earnings growth of 26% in 2021, but a shrinkage of 220% in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Megawide’s PHP 5.12 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 7% annually over the next three years. What sell-side analysts expect for Megawide’s earnings growth is above what the current stock market valuation requires in 2021, but well below the requirement in 2022.

Furthermore, the company’s earning power is below the long-run corporate average. Moreover, cash flows and cash on hand are below total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a high credit and dividend risk.

Lastly, Megawide Construction’s Uniform earnings growth is well above peer averages, and is also currently trading above its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com