With its diversification strategy, this real estate company developed stronger Uniform ROAs of 4%, not 2%

Despite belonging to one of the hardest hit sectors during the pandemic, companies in real estate have pushed forward, continuing further developments and expansion.

Specifically, this company’s ability to capitalize on its projects has helped it produce better economic value for its stockholders as shown by its higher uniform ROAs.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Filinvest Development Corporation (FDC:PHL) has come a long way from its early years of buying and selling second hand vehicles. Apart from its financial and banking services through East West Banking Corporation, Filinvest engages in real estate development and leasing.

In 1967, the Gotianun family entered the real estate business as they developed subdivisions through the Filinvest Realty Corporation.

Similar to FDC, the real estate business continued its diversification strategy for its portfolio to generate stable and recurring revenues for the company.

After over 50 years of operations, the Gotianun family became one of the largest real estate developers in the Philippines. Now, Filinvest Land, Inc. (FLI:PHL) offers a wide range of products such as condominium buildings, farm estates, and industrial parks.

One of the things that made Filinvest Land stand out amongst competitors over the years is the pricing of its products that accommodate multiple income segments.

In particular, the company’s residential projects are categorized as Socialized, Affordable, Middle-income, and High-end housing. With this strategy, Filinvest Land was able to capitalize on the residential market sector as it profits from more than one source.

However, being in a highly cyclical industry, the company’s sales were still affected by the pandemic.

In 2020, real estate sales declined primarily due to slower construction activities, which lowered the percentage of completed projects that were supposed to sell. Meanwhile, revenue collections declined as well because payment due dates were extended in compliance with according to the government’s Bayanihan Act.

Despite a seemingly weak real estate market, Filinvest Land took this opportunity to capitalize on its projects to prepare itself for the return to a pre-pandemic environment.

In 2021, the subsidiary of Filinvest Land was publicly listed as a real estate investment trust (REIT) company, also known as Filinvest REIT Corp. (FILREIT).

While FILREIT accesses additional funds from investors to develop its real estate business, FILREIT is able to expand the value of Filinvest Land’s leasing business, particularly its office properties.

With Filinvest Land’s diversification initiatives to capitalize on the incentives lined up in the growing real estate industry along with its reputation through 50 years, one would expect the company has been successful in producing economic value for its stockholders.

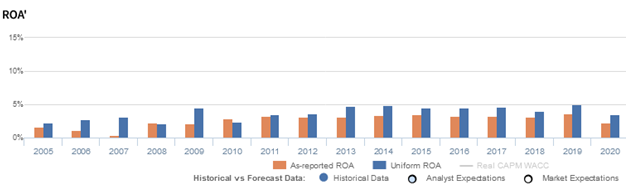

Yet, looking at as-reported metrics, it appears that Filinvest Land continues to struggle, with return on assets (ROAs) only reaching 2% in 2020.

In reality, Uniform Accounting shows that Filinvest Land’s initiative to diversify its business has generated better returns, with Uniform ROAs reaching near cost of capital levels at 4%.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

Specifically, in 2020, Filinvest Land recorded interest expenses at PHP 3.1 billion. Adding back this expense because it is not an operating expense, along with many other necessary adjustments made by Valens, leads to a PHP 5.3 billion Uniform Earnings and a 4% Uniform ROA, higher than its PHP 3.7 billion as-reported net income and 2% as-reported ROA.

Filinvest Land’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight, especially with recent years showing below cost-of-capital returns.

Filinvest Land’s Uniform ROA has actually been higher than its as-reported ROA in the past fifteen years. For example, as-reported ROA was 2% in 2020, but its Uniform ROA was actually higher than that at 4%, making the company appear to be a much weaker business than real economic metrics highlight for the past sixteen years.

Moreover, Uniform ROA expanded from 2%-3% levels in 2005-2008 to 4%-5% levels where it currently sits at the lower end of the range due to the impact of the pandemic.

Filinvest Land’s earnings margin is weaker than you think

Trends in Uniform ROA have been primarily driven by trends in Uniform earnings margin. Since 2005, Uniform margins have been significantly lower than as-reported EBITDA margins each year.

As-reported EBITDA margins declined from 29% in 2005 to 17% in 2007, before expanding to 44% levels in 2008. Then, as-reported EBITDA margins fell to 37% in 2014, before recovering to 49% in 2020.

Meanwhile, Uniform margins improved from 21% in 2005 to 34% in 2007, excluding an outperformance of 33% in 2009, Uniform margins compressed to 15% in 2010. Thereafter, Uniform margins gradually rose to 32% in 2020.

Looking at the firm’s margins alone, as-reported metrics are making the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and Filinvest Land, Inc. Tearsheet

As our Uniform Accounting tearsheet for Filinvest Land, Inc. (FLI:PHL) highlights, the company trades at a Uniform P/E of 26.3x, above the global corporate average of 24.0x, and its historical P/E of 19.6x.

High P/Es require high EPS growth to sustain them. In the case of Filinvest Land, the company has recently shown a 58% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Filinvest Land’s sell-side analyst-driven forecast is to see Uniform earnings shrinkage of 57% in 2021, but a 29% growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Filinvest Land’s PHP 1.10 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to decline 2% annually over the next three years. What sell-side analysts expect for Filinvest Land’s earnings growth is below what the current stock market valuation requires in 2021, but above the requirement in 2022.

However, the company’s earning power is below the long-run corporate average. Moreover, cash flows and cash on hand are below total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a high dividend risk.

To conclude, Filinvest Land’s Uniform earnings growth is well below peer averages, but currently trades above its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com