With over 2.5 billion gamers in the world, this gaming giant is set to power up its Uniform ROA to 24% levels

Video games are one of the top choices of entertainment during this time. As the demand for these rises, gaming stocks will continue to outperform the market.

This company is currently the top player in the space, even though historically, it struggled to adapt to industry trends and experienced a collapse in profitability beginning in 2008.

But by focusing on consumer wants and expanding to multiple platforms, it was able to recover to previous strong profitability levels.

Though as-reported metrics may signal that the company’s strategies may not be effective, TRUE UAFRS-based (Uniform) analysis shows that this company has actually maintained its robust profitability and is expected to see further earnings growth in the future.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

With the extension of the quarantine for a couple more weeks, people are finding themselves settling into the “new normal.”

Being cooped up at home gave people time to focus on their hobbies. Some spend their days playing video games or binge watching all day while some are exploring new hobbies like painting or learning a new language.

While the stock market took a dive due to COVID-19-related concerns, a few stocks were hit a little less brutally. As we’ve mentioned in past editions of the Philippine Market Daily newsletters, companies like Hormel (packaged food and meats) and Netflix (online streaming service) do well under the current situation. Sometimes, they might even perform better.

For this week, we’ll be focusing on stocks from an industry in the same pandemic-resilient category: gaming stocks.

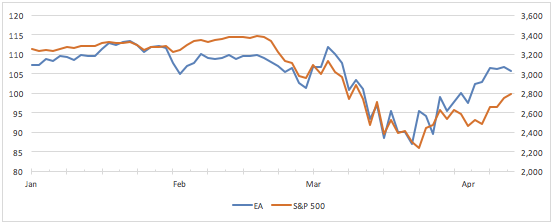

Over the past month, a number of these stocks have been outperforming the S&P 500. Included in this list are some of the biggest names in the industry—Activision Blizzard, Inc. (ATVI), Take-Two Interactive (TTWO), and Electronic Arts, Inc. (EA).

EA, specifically, has lost about 1% of its stock value since the beginning of March 2020. Meanwhile, the S&P 500 has lost about 10% over the same time frame.

The COVID-19 pandemic caused people to cancel all outside events. However, video games are about as good as any entertainment while they are confined to their homes practicing social distancing.

Although the demand for EA’s games have surged over the past month, historically, profitability has been at low levels prior to 2015.

As one of the largest global game developers, this company is known for its diverse game library. It introduced some of the world’s most popular franchises from FIFA, to The Sims, to Plants vs Zombies.

EA Sports, its sports games segment, was what led to most of the company’s success in the ‘90s to the early 2000s. It was able to update and re-release its franchises annually, with gamers patiently waiting to get ahold of the newer versions.

However, in the late 2000s, its strategy was no longer working.

With the company lacking new blockbuster titles, consumers started to suffer from franchise fatigue. This, coupled with operational inefficiencies, led to a slew of problems for the firm.

To add to its problems, this was the era when the sector was shifting to online gaming content and subscription models, and from people buying games to game reselling.

The company began having trouble keeping up with the rapid transition in the industry’s trend, which caused it to fall behind its competitors. With the then-ongoing market recession coinciding with its problems, the company’s profitability sank.

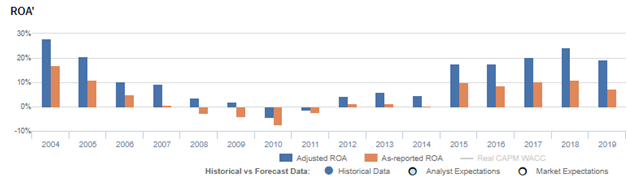

EA’s Uniform ROA fell from 20%+ levels prior to 2005 to negative levels in 2010, before recovering to modest 4%-6% levels through 2014.

Although it seemed that EA’s gaming empire had collapsed, a strategic reorganization of its segments, a culture of embracing industry trends, and strong marketing and partnership initiatives all led to a robust rebound in profitability.

EA invested heavily into online and multiplayer platforms for its main franchises. It started offering free-to-play console and mobile games, and was able to put an emphasis on in-game transactions.

The company also went into competitive gaming, such as e-sports, to capitalize on social media trends and streaming platforms.

While as-reported metrics make it seem like the company’s strategy overhaul was not as successful as it hoped and that profitability is again rolling over, Uniform Accounting would say otherwise.

Over the past five years, EA’s Uniform ROA has been in the range of 18%-25% while as-reported metrics suggest that the company’s profitability is only half of that.

The discrepancy between the two is due to the mistreatment of stock options on the income statement.

The company has had material non-cash stock option expenses relative to its earnings in the recent years. This is recorded as an expense when it should be treated as a dilution to the company’s equity, since stock options are a way for the firm to give employees an ownership stake.

Since a cash outflow is not evident in these transactions, unless the company uses cash to suppress the dilution, it would be inaccurate to deduct these expenses from earnings. Not adding back these non-cash expenses make profitability appear lower than it actually is.

This is what happened with EA. In reality, the company’s Uniform ROAs are actually 2x-3x stronger than as-reported metrics show.

However, the success of its strategy lies beyond the robust profitability levels it has achieved. To continue generating stock value, the company would need to sustain the strength of these levels.

In order to do that, EA would have to continue adapting and evolving with the ever-changing dynamics of the gaming industry.

So far, the company seems to be doing just that.

Until recently, it developed a partnership with Valve to put its games on Steam, a video game engine that caters to 90 million gamers around the world—it’s sort of like Netflix, but for games.

Not only will this boost sales, it also shows that the company is able to expand its platform reach—now catering to the popular online computer gaming community.

Furthermore, positive management sentiment points to signs of a continuation of its recent profitability trends.

Specifically, management is confident in the company’s financial and console growth. Also, they are confident in its game portfolio and how this positions the company towards new growth areas. Finally, they are confident in the opportunities that the mobile gaming market has.

Although expectations for EA are somewhat high, management’s confidence in key areas and recent strategic initiatives may justify current valuations going forward.

Electronic Arts’ earning power is still actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Uniform ROA has been higher than as-reported ROA in the past sixteen years. For example, as-reported ROA for Electronic Arts, Inc. (EA:USA) was 7% in 2019, which is materially lower than its Uniform ROA of 19%.

EA’s Uniform ROA ranged from -4% to 28% over the past sixteen years. From a historical high of 28% in 2004, Uniform ROA fell to -4% in 2010. It then recovered to 4% to 6% levels in 2012 to 2014, and then jumped to 18% in 2015. Uniform earning power grew to 25% in 2018, but declined to 19% in 2019.

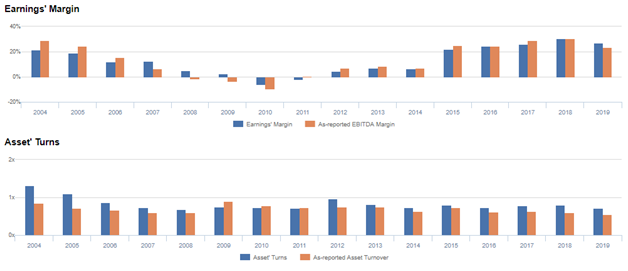

Electronic Arts’ Uniform ROA is driven by robust Uniform asset turns

Trends in EA’s Uniform ROA have largely been driven by trends in Uniform earnings margin and its stability in Uniform asset turns.

From 2004-2010, Uniform earnings margins declined sharply from 21% to -6%, before recovering to 22% levels in 2015. It then further increased to a peak of 31% in 2018 before declining to 27% in 2019.

Meanwhile, Uniform asset turns fell from 1.3x in 2004 to 0.7x in 2008. It then improved to 1.0x in 2012, before stabilizing to 0.7x to 0.8x levels through 2019.

At current valuations, markets are pricing in expectations for Uniform earnings margins to compress slightly, coupled with stability in Uniform asset turns.

SUMMARY and Electronic Arts Tearsheets

As the Uniform Accounting tearsheet for Electronic Arts, Inc. (EA) highlights, the Uniform P/E trades at 19.3x, which is below corporate average valuation levels but around its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of EA, the company has recently shown a 13% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, EA’s Wall Street analyst-driven forecast is a 36% growth in 2020, and a 14% shrinkage in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify EA’s $106 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 2% each year over the next three years. What Wall Street analysts expect for EA’s earnings growth is above what the current stock market valuation requires.

The company’s earning power is 3x the corporate average. Also, cash flows are about 3x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit risk and dividend risk.

To conclude, EA’s Uniform earnings growth is above peer averages in 2020. Also, the company is trading below average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com