With the immense popularity of streaming culture around the globe, this stay-at-home stock might actually flick past Uniform ROAs of 24%+ levels.

There is an emerging set of stocks that are successfully maneuvering around the pandemic: the stay-at-home stocks. With people in quarantine, it’s only logical that these companies benefit from the increase in demand, and subsequently, stock value.

One of these stay-at-home stocks is a streaming giant who disrupted the way people watch TV—a business that is paying off in this pandemic.

However, is this a short-term surge or a long-term tailwind to the company’s value? Uniform valuations, market expectations, and misunderstood financials hold the answer.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

It’s been weeks since the Philippine government, and other governments across the globe, mandated a quarantine and people have been cooped up in their homes ever since.

Most businesses have cut down operations while some have ceased them completely, causing stock markets around the world to decline to fresh lows from previous highs.

However, stocks like those from the consumer staples sector, were among the few stocks that were least affected by the broader market sell-off. We discussed one example in last Thursday’s Philippine Markets Daily article.

As we adjust to the new normal—or a prolonged period of self-isolation and doing practically everything at home—a new basket of coronavirus-immune stocks has also emerged: the stay-at-home stocks.

Included in this mix are companies that are expected to thrive off of the idea that people will be demanding goods and services that make outside-world activities possible without the risk of infection.

At the top of the list are e-retailers like Amazon (AMZN), perfect for at-home shopping, ZOOM (ZM) for people with work-from-home or online school setups, and at-home entertainment companies like Activision (ATVI) and Netflix (NFLX).

Netflix, in particular, saw its stock price rise by 20% from last week while the S&P 500 lost about 7% of its value over the same time frame. This period saw an increase in confirmed US coronavirus cases from 4,500 to 55,000, prompting people to quarantine themselves at home.

The move is pretty logical. With virtually all forms of outside entertainment shut down, streaming—or even binge-watching—movies and series online is one of the few home-bound entertainment channels people are leaning towards.

With over 167 million subscribers in over 190 countries, the company’s global reach is an opportunity for them to expand subscriber count to new highs.

The data shows exactly that—Netflix subscriber count has gone up in countries affected by the coronavirus.

Downloads in several countries were up from the start of the year: 33% in South Korea, 50% in France, and 100% in Italy. However, at this time, the company has decided not to comment further on the impact of the coronavirus on its revenues.

So that leaves us with the question: are these gains sustainable in the long run? The answer lies in their business model.

Netflix originally started out as a rent-by-mail DVD service with a pay-per-rental model. Unfortunately, with Blockbuster dominating the movie rental market, this business model wasn’t differentiated enough to be successful.

So they switched to a subscriber-based model which eventually switched to a streaming model, an unprecedented move that took advantage of the technological advances in the digital space.

Fast forward to the late 2000s and the company had already disrupted the way people watch movies. There was no more walking to the DVD store, no more late rental fees, no more Blockbuster.

Now, this company has become the leading subscription streaming entertainment service in the world.

However, Netflix might not be the only player in the race anymore.

People have been opting to switch out cable for a monthly subscription for video-on-demand (VOD) services. Realizing that there is a rise in demand for these services, cable companies are now following suit to keep up with this trend.

Disney, for example, recently launched Disney+. The company pulled out all of its content from Netflix, including all the movies from the Marvel Cinematic Universe, resulting in around 1 million Netflix users canceling their subscriptions.

In order to soften the blow, Netflix is planning to partner with Nickelodeon to produce new films and shows.

Even so, this might not be enough as other major companies join the VOD bandwagon, such as Apple’s Apple TV+ and WarnerMedia’s HBO Max, and are aiming to drag subscribers away from current players in the space.

So while Netflix is enjoying the short-term surge in demand while people are in quarantines and self-isolation, competitive headwinds may inhibit the company’s ability to sustain current robust Uniform return on assets (ROA) in the long-term.

Considering that, while market expectations are low, an inability to surpass these expectations and an above peer-average Uniform P/E of 39.1x may suggest that the stock is fairly valued at best.

Netflix’s earning power is still actually more robust than you think

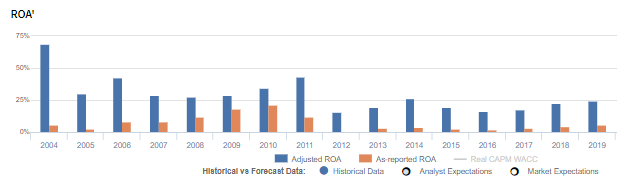

As-reported metrics significantly understate Netflix Inc.’s (NFLX:USA) profitability.

Uniform ROA has been higher than as-reported ROA in the past sixteen years. Currently, as-reported ROA is 5% in 2019, far lower than Uniform ROA of 24%. As-reported ROA is making the company look like a much weaker business than real economic metrics highlight, distorting the market’s perception of the firm’s historical profitability trends.

Moreover, as-reported ROA has increased from 2% in 2016 to current 5% levels while Uniform ROA also increased from 16% to 24% over the same period, directionally distorting the market’s perception of the firm’s historical profitability trends.

Historically, Netflix has seen robust, yet volatile profitability. After falling from 60%+ levels in 2004 to 28%-29% from 2007-2009, Uniform ROA expanded to 43% in 2011, before fading to 16% in 2012.

Since then, Uniform ROA has improved to 20%-26% levels through 2018, before stabilizing to 24% in 2019.

Netflix’s Uniform ROA is driven by robust Uniform asset turns and Uniform earnings margin

Trends in the company’s Uniform ROA have largely been driven by its stability in Uniform asset turns and trends in Uniform earnings margin.

From 2012-2018, Uniform earnings margins improved markedly from 6% to 14%, before increasing to 16% levels in 2019.

Uniform Turns have fallen from peak 7.1x levels in 2004 to 2.1x-2.6x levels from 2012-2016, which further declined to 1.5x in 2019.

At current valuations, markets are pricing in expectations for improvements in both Uniform earnings margins and Uniform asset turns.

SUMMARY and Netflix Tearsheet

As the Uniform Accounting tearsheet or Netflix highlights, the Uniform P/E trades at 39.1x, which is above corporate average valuation levels but around its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Netflix, the company has recently shown a 45% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Netflix’s Wall Street analyst-driven forecast is 38% into 2020, and 31% into 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Netflix’s $333 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 24% each year over the next three years. What Wall Street analysts expect for Netflix’s earnings growth is above what the current stock market valuation requires.

The company’s earning power is 4x corporate averages. Also, cash flows are about 3x their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit risk and dividend risk.

To conclude, Netflix’s Uniform earnings growth is above peer averages in 2020. Also, the company is trading above average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com