After a big win, this activist hedge fund has a new target

Back in 2021, we originally wrote about Starboard Value and detailed the unique structure of this activist hedge fund.

For a refresher, Starboard Value has a proven history of guiding corporate transformations that have been lucrative for investors.

Like most activist funds, it invests in companies to make changes rather than waiting for the companies to change themselves.

Today, we’ll use Uniform Accounting to look over the fund’s top 15 holdings and cover how the company has maintained its reputation in the activist market.

In addition to examining the portfolio, we include a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Also below is a detailed Uniform Accounting tearsheet of the fund’s largest holding.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Starboard Value is a notoriously successful hedge fund.

As we wrote back in 2021, the origins of the firm began with Peter Cohen, one of the most respected names in the hedge fund universe.

After consolidating investment banking and hedge fund operations under Cowen & Company, Cohen sought to introduce a different approach for this new conglomerate.

Cohen always had a sharp eye for talent, and so in 2002, he helped found an activist investor firm within Cowen, which eventually became Starboard Value.

Activist companies adopt a strategy for investing that is far more aggressive than that of traditional hedge funds. They make an effort to exert influence over a company’s management through investments, pressuring, or even threats of a takeover to certain actions.

These moves can force management teams to put short-term profitability ahead of long-term growth, which inherently counteracts the motive to create shareholder value. Elliott Management, one particular fund that we’ve previously reported, has a tendency to threaten to use its voting power to produce hit pieces on the company CEOs.

These “hit pieces” and discussions are often unveiled in the 13D filings.

For context, the 13D form is essentially the activist investor’s campaign announcement. In these filings, investors are able to outline the strategy and proposed changes for the target company.

These disclosures may often warrant discussion among the two parties on the proposals, especially if the target company does not want a fund to purchase a stake in the company.

This was evidenced by Netflix (NFLX) when Carl Icahn attempted to purchase 10% of the popular streaming company. Both parties fueled a discussion through amended 13D filings.

Despite the unconventional strategies and bad rap the activist space has made for itself, it is without a doubt that companies like Starboard are generating impressive profits.

The company seems to have mastered the activist strategy and found effective ways to leverage its minority stakes. The returns are there for evidence.

Even in its earlier stages, it was reported that 80% of Starboard’s activist campaigns were profitable.

Additionally, Starboard has made 111 13D filings, with a return average of 27.52% compared to the S&P 500’s 12.10%, all recorded within the same time period.

Starboard’s notable deals include pushing AOL to fundamentally change its operations in 2011 and orchestrating the OfficeMax and Office Depot merger in 2013.

As of 2023, the fund continues to experiment in the space.

Most recently, Starboard acquired a 7.5% stake in Algonquin Power (AQN). The premise of the acquisition was the funds’ belief that the “sale of Algonquin Power’s renewables business can help it reduce leverage and provide a safer dividend.”

This play is different from its historical track record as this is the first utility company that Starboard has filed for.

Additionally, the company has recently made news with the sale of one of its top holdings, Splunk (SPLK), to Cisco Systems (CSCO) as well as its interest in GoDaddy (GDDY).

Starboard has a large stake in GoDaddy tracking back to 2021. However, In a recent letter, Starboard stated it is “disappointed by GoDaddy ‘s operational, financial, and stock price performance.” Also hinting at the idea of a potential sale of the company if they are not able to generate shareholder value and improve Starboard’s board presence.

Evidently, the fund hasn’t changed its strategy since we first looked at them in 2021. The returns are there and Starboard continues to remain prevalent in its activist campaign.

That said, let’s take a look at Starboard’s top 15 holdings and see if any of its activist prospects show promise in the future.

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It’s no surprise that once many of these distortions are accounted for, it becomes apparent which companies are in real robust profitability and which may not be as strong of an investment.

See for yourself below.

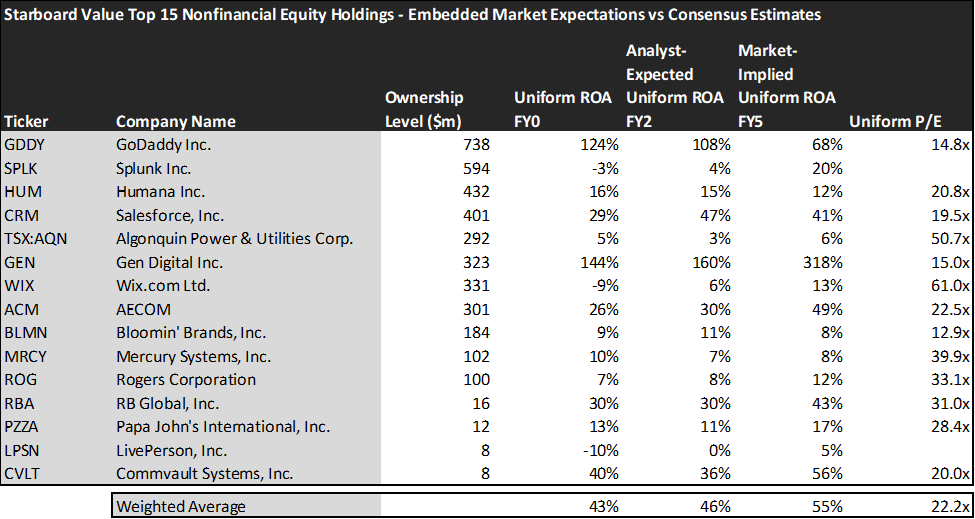

Looking at as-reported accounting numbers, investors would see that the Starboard Value invests in very low-quality companies.

On an as-reported basis, many of the companies in the fund are notably below-average performers. The average as-reported ROA for the top 15 holdings of the fund is 2%, which is significantly lower than the 12% U.S. corporate average.

However, once we make Uniform Accounting adjustments to accurately calculate the earning power, we can see that the average return of Starboard Value’s top 15 holdings is significantly more profitable than what as-reported metrics show, which is coming in at 43%.

As the distortions from as-reported accounting are removed, we can see that GoDaddy Inc. (GDDY) isn’t a 4% return business. Its Uniform ROA is 124%.

Meanwhile, Salesforce, Inc. (CRM) seems like a 1% return business, but this software company actually powers a 29% Uniform ROA. That being said, to find companies that can deliver alpha beyond the market, just finding companies where as-reported metrics misrepresent a company’s real profitability is insufficient.

To really generate alpha, any investor also needs to identify where the market is significantly undervaluing the company’s potential.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The average Uniform ROA among Starboard Value’s top 15 holdings is actually 43%, which is way above the corporate average in the United States.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here are 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, the average Uniform P/E across the investing universe is roughly 20x.

Embedded Expectations Analysis of Starboard Value paints a clear picture. Over the next few years, Wall Street analysts expect the companies in the fund to remain relatively at the same levels of profitability. Similarly, the market has expectations for these companies to stay on track with current valuations.

Analysts forecast the portfolio holdings on average to see Uniform ROA slightly jump up to 46% over the next two years. At current valuations, the market has lower expectations than analysts and it expects a 55% Uniform ROA for the companies in the portfolio as well.

For instance, Bloomin’ Brands, Inc (BLMN) returned 9% this year. Analysts anticipate its returns to increase to 11%. The market seems to think almost the same about the company’s future and its pricing in a slight decrease in profitability to reach a Uniform ROA of 8%.

From a universal standpoint, it’s evident that the fund prioritizes the selection of financially sound and profitable businesses. Several companies in the fund’s top holdings are powering ROA’s above 30% which is exceptional relative to the corporate average.

Looking at the entire portfolio, market expectations and current valuations are in line which suggests that the stability of these companies is already being priced in. This could possibly limit the upside for investors and would require these companies to notably exceed expectations.

However, a complete understanding of this portfolio requires an analysis of the activist nature of the fund. This hedge fund must be seen in a different light.

The company is mainly invested in its activist campaigns and generating shareholder value for undervalued companies. This principle is apparent considering the recent sale of its 2nd largest holding, Splunk Inc. (SPLK).

Starboard has been holding Splunk for a year as it viewed it as a valuable acquisition target, investing in a 2.46% stake. Similar to how Starboard handles most of these positions, the company pushed and enacted initiatives to improve the company’s growth and profitability.

In fundamentally improving the business, with the help of other stakeholders, the company earned the attention of cybersecurity giant Cisco Systems (CSCO) who closed a $28 billion dollar deal with Splunk. With its 2.46% stake in Splunk and premium selling price, Starboard managed to generate a rumored 85% return on the investment. Situations like these are where this fund is able to generate returns and how the fund should be evaluated by investors.

Moreover, the funds’ future performance may be heavily correlated with the potential it can extract from its top holding, GoDaddy (GDDY). In a similar scenario, Starboard currently holds 7.8% of GoDaddy, its third-largest shareholder.

With Starboard having high stakes in GoDaddy, investors should pay close attention to the outcome of the dispute between GoDaddy’s management and Starboard’s desire for a stronger board presence.

At the end of the day, Starboard has proven to remain resilient in its activist campaigns. This alternative type of investment strategy could be interesting to one’s portfolio.

If so, investors should look beyond the numbers and understand the underlying goals in each of Starboard’s holdings.

This just goes to show the importance of valuation in the investing process. Finding a company with strong profitability and growth is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which have upside which has not been fully priced into their current prices.

To see a list of companies that have great performance and stability at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of one of Starboard Value’s largest holdings.

SUMMARY and GoDaddy Inc. Tearsheet

As one of Starboard Value’s largest individual stock holdings, we’re highlighting GoDaddy Inc. (GDDY:USA) tearsheet today.

As the Uniform Accounting tearsheet for GoDaddy Inc. highlights, its Uniform P/E trades at 14.8x, which is below the global corporate average of 18.4x, and its historical average of 17.6x.

Low P/Es require low EPS growth to sustain them. In the case of GoDaddy Inc., the company has recently shown 30% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, GoDaddy Inc.’s Wall Street analyst-driven forecast is for EPS to shrink by 3% in 2023 and to grow by 19% in 2024.

Furthermore, the company’s return on assets was 124% in 2022, which is 21x the long-run corporate averages. Also, cash flows and cash on hand exceed its total obligations—including debt maturities and CAPEX maintenance. These signal moderate operating risk and moderate credit risk.

Lastly, GoDaddy Inc.’s Uniform earnings growth is in line with peer averages, and in line with peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research