Uniform Accounting can uncover the mystery behind Bridgewater’s underperformance

The turmoil in U.S.-listed Chinese stocks over the past year or so, during which time some companies’ share prices have declined by more than 50%, came as no surprise to those who have long warned of the perils of investing in China’s not so open market.

Yet, even as political and economic conditions in the country deteriorate further, long-time China bull Ray Dalio and his $160 billion dollar hedge fund Bridgewater Associates remain unphased.

Is exposure to China the reason Bridgewater’s flagship funds have been underperforming lately? Or is there something deeper going on beneath the surface of Wall Street’s most secretive money manager?

Today we’ll look at Bridgewater’s top individual company holdings through the lens of Uniform Accounting to find out.

In addition to examining the portfolio, we’re including a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Larry Fink and his colossal empire at BlackRock aren’t the only asset managers who’ve been called out by peers lately for their commitment to remaining bullish on China, even in the face of what seems to be an endless list of worries.

First and foremost among these concerns is the brewing default of Evergrande Group (3333:HKG), the world’s most indebted property developer, and its potential impact on the multi-trillion dollar Chinese property market.

As we highlighted last week, we believe the pending collapse of Evergrande is not a Lehman moment for China, though the build up of debt in corners of the Chinese market and an overreliance on housing to fuel growth are long standing causes for concern.

Secondly, and perhaps more importantly, are the shifting political winds in Beijing under President Xi Jinping, something we’ve also discussed before.

A series of crackdowns on internet technology companies and the private education industry have erased billions of dollars of market capitalization from U.S.-listed Chinese companies, leading many to view Xi’s China as an increasingly anti-free market.

With the CCP’s assertion of increased state control over the private economy and its nascent push for “common prosperity,” a catch all phrase for reducing income inequality, the thesis of China as a hostile location for foreign investors seems to be playing out just as many of the bears have suggested.

Add to these concerns a recent slowdown in growth due to localized outbreaks of COVID-19, an increase in energy shortages as the country moves to meet its climate goals, and persistent demographic challenges associated with the disastrous one-child policy and you have what appears to be a bleak outlook for the future.

Nevertheless, billionaire hedge fund mogul Ray Dalio and his firm, Bridgewater Associates, remain long-term bulls on China.

Founded out of a two-bedroom apartment in New York City in 1975, Bridgewater has grown to become the world’s largest hedge fund, with over $160 billion in assets under management.

From the very beginning, Dalio has been an outspoken advocate of investing in China. Since the late 1980s, when he was first brought to the country as an informal advisor to help set up China’s stock markets, Dalio has maintained personal relationships with Chinese officials at the highest levels.

In fact, his connections run so deep that his son Matt, who spent much time as a child in China learning the language and culture, established a charitable foundation for special-needs orphans at only 16 years old.

It is therefore unsurprising that Dalio and Bridgewater were one of the first American hedge funds allowed access to the Chinese market, taking in funds from institutional investors and wealthy Chinese individuals.

Not only does Bridgewater do business in China, but the fund also invests in some of the country’s largest companies, particularly e-commerce giant Alibaba (BABA).

Yet, the lackluster performance of late has led many to wonder if Dalio’s obsession with China is merely another blunder, adding to a losing streak that has seen poor returns and a warning from the $20 billion Orange County Employees Retirement System that it may dump the firm’s flagship Pure Alpha fund.

For quite some time, Dalio and Bridgewater were viewed as the gold standard for quantitative, macro-driven hedge funds, as we highlighted in our review of the firm’s ultra-secretive investment strategy last January.

Today, however, one can’t be blamed for wondering if Bridgewater’s approach is creating more issues than success for the company. That’s why taking a look at the fund’s portfolio using Uniform Accounting is particularly relevant, to make sure it hasn’t lost course.

Because its numbers-driven strategies are all hedged and designed to balance risk and reward, some of its biggest holdings are ETFs that track indices such as the S&P 500. On the surface, this doesn’t offer us much insight into the firm’s capabilities.

However, if we look at the fund’s largest non-financial, individual company holdings, we can see the stocks Ray Dalio’s process has identified to generate alpha.

Take a look for yourself…

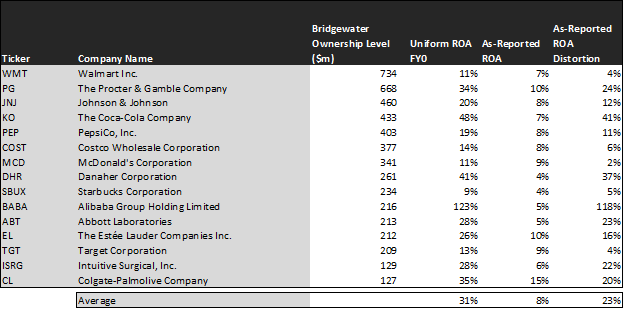

Relying on as-reported metrics, it would appear the struggles at Bridgewater are real, as the average return on assets (“ROA”) for companies in its portfolio is a meager 8%, well below U.S. averages of 12%.

This suggests the world’s biggest hedge fund is losing out by investing heavily in China and other quantitatively selected firms, rather than betting on the U.S. economy alone.

In reality, by utilizing Uniform Accounting we can see the picture isn’t so bleak. With innovative companies like Alibaba and Intuitive Surgical (ISRG), whose Uniform ROAs are 123% and 28% respectively, along with cash-generating stalwarts such as The Coca-Cola Company (KO), the portfolio’s average Uniform ROA is actually 31%, not 8%.

This is because Generally Accepted Accounting Principles (GAAP), the rulebook companies must follow when reporting their performance, has many fundamental flaws. Here at Valens, we have made it our mission to cut through that noise to deliver a real, consistent representation of corporate profitability through our Uniform Accounting framework.

However, just finding innovative companies with strong economic productivity isn’t enough to make them investible. To truly unlock alpha, investors need to find companies that are more productive than the market realizes.

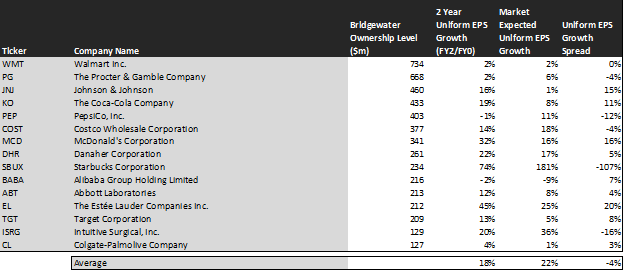

Looking at the chart below, which uses our embedded expectations framework to see what the market is pricing in, we can discover if investors are rewarding the true profitability these companies exhibit, or if there are some major mispricings.

This chart shows three interesting data points:

– The first datapoint is what Uniform earnings growth is forecast to be over the next two years when we take consensus Wall Street estimates and convert them to the Uniform Accounting framework. This represents the Uniform earnings growth the company is likely to have over the next two years.

– The second datapoint is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we are showing how much the company needs to grow Uniform earnings to justify its current stock price. If you’ve been reading our daily newsletters and our reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for Uniform earnings growth.

– The final datapoint is the spread between how much the company’s Uniform earnings could grow if Uniform Accounting adjusted earnings estimates are correct, and what the market expects Uniform earnings growth to be.

With analyst forecasted average earnings growth of 18% versus priced-in expected earnings growth of 22%, it appears Bridgewater’s holdings are being overvalued by the market.

The standout name here is Starbucks (SBUX). The market is pricing in a massive 181% increase in earnings per share (“EPS”) over the next two years, but analysts are only forecasting Uniform EPS to grow by 74% over the same timeframe.

This suggests the coffeehouse chain may be significantly overpriced, with little room left to exceed market expectations and drive share prices higher.

Similarly, robotic surgical equipment producer Intuitive Surgical, creator of the revolutionary Da Vinci Surgical System, has a priced-in earnings expansion of 36%. Meanwhile, analysts covering the company believe earnings will only expand by 20% over the next two years.

Taken as a whole, a Uniform Accounting spotlight suggests Bridgewater’s recent underperformance may have something to do with the strategy failing to find mispricings and instead holding expensive names.

Moreover, Dalio’s bullishness on China may also be playing a significant role, given the firm’s large position in Alibaba.

Despite the e-commerce giant’s innovativeness and opportunities in areas like cloud computing and entertainment, the broad tech crackdown of the past few months has led both the market and analysts to re-level their expectations for the company.

Though it has a robust Uniform ROA of 122%, the market is pricing earnings growth to actually decline by 9% over the next two years, while analysts are also projecting a less severe decline of 2%.

As long as Bridgewater remains committed to equities in China, it runs the risk of continuing to underperform if political headwinds worsen and forecasts for negative earnings growth become reality.

While one of the hedge fund world’s biggest names has developed a strategy that can find profitable companies, despite what GAAP may suggest, Uniform Accounting shows us that Bridgewater’s weakness may lay in its ability to get pricing and geopolitical risk right.

SUMMARY and Walmart Inc. (WMT:USA)

As one of Bridgewater’s largest individual stock holdings, we’re highlighting Walmart’s tearsheet today.

As the Uniform Accounting tearsheet for Walmart Inc. (WMT:USA) highlights, its Uniform P/E trades at 25.7x, which is around the global corporate average of 24.3x and its own historical average of 25.1x.

Moderate P/Es require moderate EPS growth to sustain them. In the case of Walmart, the company has recently shown a 37% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Walmart’s Wall Street analyst-driven forecast is for EPS to shrink by 14% in 2022, but grow by 22% in 2023.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify Walmart’s $139 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 1% annually over the next three years. What analysts expect for Walmart’s earnings growth is below what the current stock market valuation requires for 2022, but above that requirement in 2023.

Furthermore, the company’s earning power is 2x long-run corporate averages. Moreover, cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. Moreover, intrinsic credit risk is 20bps. Together, these signal a low credit and dividend risk.

Lastly, Walmart’s Uniform earnings growth is below its peer averages, but the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research