Why the Fed’s focus on inflation matters to equity markets

Inflation is a key part of equity market valuations. Without an ear to the ground on inflation, it’s easy to lose money at any stage in the market.

The consequences of inflation have entered the public discourse once again as the yield curve has spiked and Jerome Powell has spoken about inflation to congress. With fears of stimulus leading to excessive inflation, we are breaking down the risk to the markets.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

In late February, the chair of the Federal Reserve, Jerome Powell, testified before the Senate and the House of Representatives.

Under the Humphrey-Hawkins Act, a sitting chair must report on monetary policy to the Senate and House Banking Committee.

In recent testimonies, the Fed Chair reported on all matters of economic policy, from employment to tax cuts or stimulus spending.

As this is a chance for senators and members of Congress to show their constituents they are making sure the Fed is watching out for them, a Fed Chair usually gets questions about how their policies will directly impact the concerns of the voters.

So it was interesting that this time up on the Hill, Powell was asked about little other than inflation.

As this CNBC article highlights, Powell stated inflation and employment remain well below the target the Federal Reserve has set. He also said the Fed is “committed to using our full range of tools…to help ensure the recovery from this difficult period will be as robust as possible.”

Powell explicitly talked about how inflation was still “soft,” and the Fed would be sure to avoid a situation like the 1970s. Back in 2019, we talked about how double-digit inflation in the ‘70s suppressed stock values.

These concepts still ring true today. High inflation means investors lose out on returns, and folks everywhere lose buying power.

However, Jerome Powell’s assurances come at a time of low inflation. Over most of the past 7 years, inflation has been below 2%. Inflation even approached 0% during the worst part of the pandemic.

This messaging might have you scratching your heads. After all, it would seem a plethora of other economic problems should be higher on the Fed’s radar. This comes back to an indicator we talked about last week.

As we discussed last Monday, many pundits view the sharp rise in 10-year Treasuries as the markets hunkering down for high inflation. It’s not just the yield curve that warns about this possibility, though.

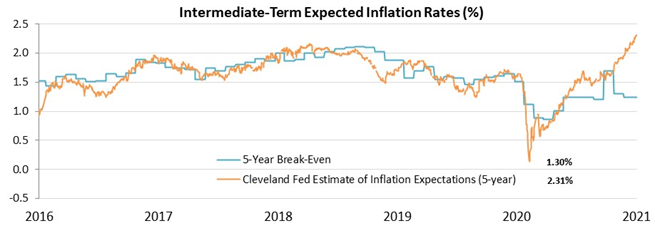

The Cleveland branch of the Federal Reserve tracks an expected inflation rate over different time periods, using a variety of inflationary signals.

At the beginning of 2020, the Cleveland Fed put inflation expectations on the low end of five-year levels. However, by February of 2021, inflation expectations have reached five-year highs.

There are a number of factors leading to this expectation for rapidly increasing inflation.

The first is the central bank has opened the monetary floodgates, and the government’s prior and future stimulus plans involve literally sending taxpayers money. Policy makers clearly are prioritizing keeping employment high rather than taming inflation.

Furthermore, while the economy is now hampered, the promise of easing quarantine restrictions promises to boost spending.

With so many saving their cash for vacations, spa trips, or just dining out after quarantine is lifted, more cash chasing the same goods threatens inflation. Meanwhile, as supply chain disruptions become untangled, supply constraints could drive prices even higher.

Altogether, these factors lead to a probability of higher inflation going forward.

It is important to keep in mind this inflation is not going to strangle the economy like in the 1970s. Inflation is starting from multi-decade lows.

Most likely, inflation will rise from the 1.5% to 2% levels of the past five to seven years to around 2% to 2.5%. Were the Fed to really allow things to heat up to ensure economic recovery, inflation rates may even hit 3%.

This is leagues below the Senate’s fears of a return to 1970s inflation of 15% or more.

Still, any amount of inflation may impact your portfolio.

No matter what the inflation rate is, investors should always keep an ear to the ground to understand how it can impact stock prices.

Inflation directly impacts the stock market, as it distorts the discount rate for any asset. For example, inflation reached 15% in 1980. Even though the Dow Jones gained 15% that year, investors took home a “real” (meaning inflation-adjusted) return of 0% as their money only kept up with inflation.

If investors take home less during a period of high inflation, they are not willing to pay as much for cash flows out in the future. This in turn crushes valuations.

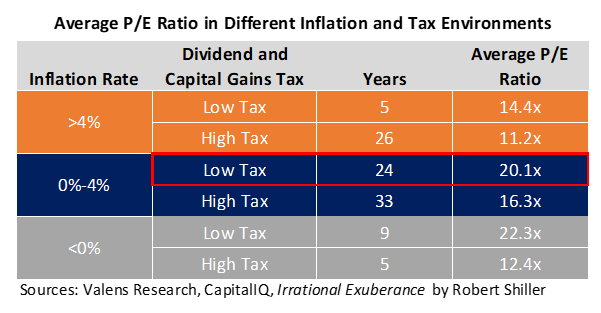

In the table below, we can directly see how low and high inflation environments impact valuations. In times where inflation is over 4%, average P/E ratios are between 11.2x and 14.4x… while during periods with moderate inflation, these ratios range between 16.3x and 20.1x.

This trend is exacerbated for growth companies, as most of the value of these companies is tied up in cash flows that are coming years out. As that cash flow becomes less valuable today, it can lead to the big swings in valuations we saw in the last two weeks.

So it is no surprise that as Powell was giving his presentation to the Senate, high growth technology and biotech came under selling pressure.

This risk of inflation and more are discussed in our publication The Market Phase Cycle which details the current macroeconomic conditions. This way, investors can make the right asset allocation decisions with their clients’ money.

If you want to read more about how factors like inflation, taxes, and more affect valuations, you can read here.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research