Introducing end-to-end fiber internet shaped this company to be the fastest-growing internet provider, leading the industry with an 11% Uniform ROA

The internet has come a long way since it became commercially available in the late 1980s. Today, it is a crucial element in transforming businesses, education, entertainment, and social interactions. However, some countries such as the Philippines, still face an inferior state of internet connectivity.

Today’s company is currently one of the internet providers in the country that aims to overcome these connectivity issues by providing the first pure end-to-end fiber internet network. Although this company has generally seen declining profitability, it’s not as weak as what as-reported metrics portray.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Data analytics company Statista estimates that as of January 2021, there are about 4.66 billion active internet users, which is more than half of the global population.

However, accessibility to high-quality internet connection still has a long way to go worldwide.

Based on the latest Speedtest Global Index conducted by Ookla, Singapore is ranked number one in terms of fixed broadband speed with download rates of about 238.59 Mbps. Meanwhile, the Philippines ranked 92nd in the same category with only 38.46 Mbps.

In addition to relatively low-quality internet connection, the Philippines’ internet services are also expensive. That is why internet accessibility remains a subject of debate and complaints in the country.

One of the main factors why it’s difficult to provide fast internet for the country is the tedious process of building cell towers given the layers of bureaucracy one has to surpass. For instance, acquiring the required approved permit from 25 to 30 local government units (LGUs) usually takes around eight months just for one cell site.

Another additional contributing factor to the country’s unreliable internet service is the industry’s virtual duopoly.

For a long time, Philippine Long Distance Telephone Company and Globe Telecom have been dominating the telecommunications market. Other competitors in the space are much smaller and are only limited to fixed broadband.

Fortunately, another company has recently taken the spotlight as one of the fastest growing internet service providers.

Established in 2012, Converge ICT Solutions, Inc. (CNVRG:PHL) provides solutions to prolonged connectivity issues. The company is the first telco company that offers pure end-to-end fiber internet, a premium connection that ensures no loss in data transmission or slowdown in connectivity.

Converge also gradually trumps geographic hindrances by continuously expanding its coverage and reaching unserved and underserved areas across the country.

The company is currently pursuing this initiative by expanding its fiber footprint not only in Luzon, but also in Visayas and Mindanao through submarine cables that will link those areas with a fiber internet connection.

Furthermore, Converge introduced the country’s first 400Gbps backbone to augment the existing network capacity. This milestone is a major breakthrough that should also further meet the increasing demand for reliable internet services.

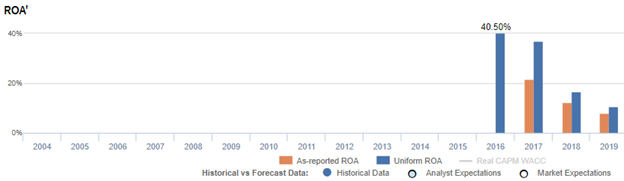

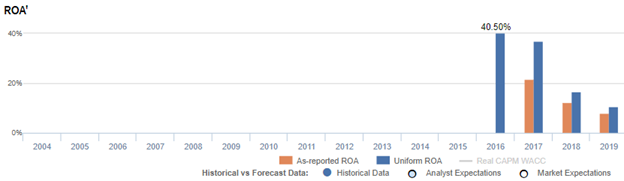

Overall, Converge’s ability to offer superior products make it seem that the company has been generating robust profitability. However, looking at as-reported metrics, it appears that these have only helped produce modest returns, with return on assets (ROAs) falling to 8% levels in 2019.

In reality, Uniform Accounting shows that although Converge has generally seen declining profitability, it’s not as weak as what as-reported metrics portray, with a Uniform ROA of 11% in 2019.

One of the factors for such a discrepancy is the failure of as-reported metrics to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

When excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

In 2019, Converge recognized an excess cash of PHP 5.5 billion, which is 18% of its as-reported total assets of PHP 31.2 billion.

After removing excess cash from the asset base and with the many necessary adjustments Valens makes, we arrive at a Uniform ROA of 11%.

Converge’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that Converge’s profitability is weaker than real economic metrics have highlighted.

In reality, Converge’s true profitability has been higher than its as-reported ROA for the past three years. Specifically, as-reported ROA was 8% in 2019, but Uniform ROA was higher at 11%.

As-reported ROA gradually declined from 22% levels in 2017 to 8% in 2019. Meanwhile, Uniform ROA compressed from 37% levels to 11% in the same timeframe.

Converge’s asset efficiency is better than you think

Similarly, as-reported metrics significantly distort the firm’s asset efficiency, a key driver of profitability.

From 2016-2019, as-reported asset turnover declined from 0.7x to 0.3x, while Uniform turns only declined from 1.0x to 0.7x, making the company appear to be a less efficient business than real economic metrics reveal.

Moreover, as-reported asset turnover has been lower than Uniform turns in each of the past four years, distorting the market’s perception of the firm’s historical asset efficiency level.

SUMMARY and Converge ICT Solutions, Inc. Tearsheet

As the Uniform Accounting tearsheet for Converge ICT Solutions, Inc. (CNVRG:PHL) highlights, it trades at a Uniform P/E of 26.0x, around the global corporate average of 25.2x, but above its historical average of 7.6x.

Moderate P/Es require moderate EPS growth to sustain them. In the case of Converge, the company has recently shown a 21% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Converge’s sell-side analyst-driven forecast calls for a 140% and 50% Uniform EPS growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Converge’s PHP 18.40 stock price. These are often referred to as market embedded expectations.

Converge is currently being valued as if Uniform earnings were to grow 47% annually over the next three years. What sell-side analysts expect for Converge’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

The company’s earning power is twice the long-run corporate average. Also, cash flows and cash on hand are almost 3x its total obligations—including debt maturities and capex maintenance. Together, this signals a low credit risk.

To conclude, Converge’s Uniform earnings growth is the highest among peers in 2020, and trades above its average peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com