Despite creating self-sustaining communities in the country’s premier locations, this company still had negative margins, not 33% per as-reported

Self-sustaining communities have been a common trend for the top property developers in the Philippines.

Like Shang Properties (SHNG:PHL), this real estate company focused on building luxurious properties and communities in some of the key locations in the Philippines. However, as-reported metrics seem to be overstating the success of its strategy.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earning Tearsheets – Philippine-listed Focus

Powered by Valens Research

More commonly known as the owner of the Manila Electric Company (MER:PHL), the Lopez family owns a 15.5 hectare of land at the heart of one of the most affluent cities in the Philippines—Makati.

This specific stretch of land was formerly used as a thermal power plant in the 1950s. However, the plant was destroyed after it was hit by a massive fire in 1973.

Due to protests against its reopening, the plant was permanently decommissioned, and the Lopez family transformed the land into a self-sustaining community. This transformation is now known as the Rockwell Center, which is the flagship development of Rockwell Land Corporation (ROCK:PHL).

Also known as a “city within a city,” the Rockwell Center is a mixed-used development that caters to upscale clients seeking an ideal residential community that puts value on well-being.

Before venturing into hotel and leisure, the company was mainly engaged in residential and commercial development with 85% of its total revenues coming from residential developments and 12% coming from commercial development. Under this segment, Rockwell Land was able to build some of the most luxurious residential condominiums in the country—such as The Grove, Proscenium, and the Arton—to name a few.

To further expand its market reach and capture residential condominium demand, Rockwell Land also delved into the affordable market by developing Rockwell Primaries in 2012.

This project focuses on offering clients a more affordable way of experiencing its high-end living spaces and communities through 53 Benitez in New Manila and the Vantage at Kapitolyo in Pasig City.

Besides capitalizing on the strong demand in urban cities, the company also saw demand strengthen in provincial cities. It then decided to expand and develop more mixed-use projects in other key cities.

Some of its projects include the Aruga Resort and Residences in Cebu and Nara Residences in Bacolod. As part of this initiative, Rockwell Land also partnered with TGN Realty in order to gain a foothold in Angeles City, Pampanga in 2020.

With a purpose of developing a 3.6-hectare mixed-use community, the Angeles project will have three residential towers that will bring in PHP 6.7 billion worth of residential inventory. This will be complemented by a retail component, which is poised to be the Power Plant Mall of Angeles—the first Rockwell mall outside Metro Manila.

Focusing on creating opulent communities through building a diverse set of portfolio in the Philippines has been emphasizing the success of Rockwell Land’s luxury brand. Looking at the company’s as-reported metrics, it seems that the company was able to benefit from this strategy, with margins reaching a peak of 33% in 2020.

In reality, its exclusivity wasn’t able to generate enough profitability as Uniform margins actually peaked at only 11% in 2019 and even fell to negative levels in 2020.

One of the most significant distortions between as-reported and Uniform metrics pertains to the treatment of equity investment income.

Equity investment income is the income arising from the company’s long-term investments classified under the equity method. It includes stocks, associates/affiliates, partnerships, and/or joint ventures.

Since equity investments are entities that the company has less than 50% control of, they are not generally considered significant to the company’s core operations. As such, equity investments and its related earnings are removed from the company’s financials.

In 2020 alone, Rockwell Land reported PHP 1.08 billion in equity investment income, which made up 90% of the company’s PHP 1.19 billion as-reported net income.

Reversing this distortion and applying the other necessary adjustments Valens makes, Rockwell Land’s 32.5% as-reported EBITDA margin and PHP 1.1 billion net income are adjusted to reveal a TRUE Uniform earnings margin of -3% and Uniform earnings of just PHP 361.7 million.

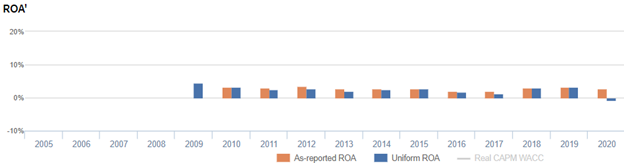

Rockwell Land’s earning power is weaker than you think in most years

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that Rockwell Land’s profitability is stronger than what real economic metrics highlight in most years.

In reality, Rockwell Land’s true profitability has generally been lower than its as-reported ROA in most years. Specifically, as-reported ROA was 3% in 2020, but Uniform ROA was -1% that year.

As-reported ROA expanded from 3% levels in 2009-2010 to a high of 4% in 2012, before gradually declining to 2% levels in 2016-2017. Thereafter, as-reported ROA has recovered to 3% levels in 2018-2020.

Meanwhile, after declining from a 5% peak in 2009 to 1% in 2017, Uniform ROA improved to 3% levels in 2018-2019 before fading to negative levels in 2020.

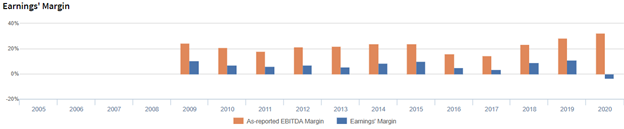

Rockwell Land’s margins are weaker than you think

Trends in Uniform ROA have been primarily driven by trends in Uniform earnings margin. However, Uniform margins have been much lower than as-reported EBITDA margins in each of the past twelve years.

As-reported margins declined from 25% in 2009 to 18% in 2011, before expanding to 24% levels in 2014-2015. Then, as-reported margins fell to a low of 15% in 2017 before elevating to a high of 33% in 2020.

Meanwhile, after fading from 11% in 2009 to 6%-7% levels from 2010-2013, Uniform margins increased to 10% in 2015. Thereafter, Uniform margins then decreased to 4% in 2017 before recovering to 10% in 2019. Afterwards, Uniform margins fell to negative levels in 2020.

Looking at the firm’s margins alone from 2009-2020, as-reported metrics make the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and Rockwell Land Corporation Tearsheet

As the Uniform Accounting tearsheet for Rockwell Land Corporation (ROCK:PHL) highlights, it trades at a Uniform P/E of 23.6x, around the global corporate average of 23.7x, but above its historical average of -8.4x.

Average P/Es require average EPS growth to sustain them. In the case of Rockwell Land, the company has recently shown a 1,347% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Rockwell Land’s sell-side analyst-driven forecast calls for a 96% and a 160% Uniform EPS decline in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Rockwell Land’s PHP 1.55 stock price. These are often referred to as market embedded expectations.

The company’s earning power is below the long-run corporate average. However, cash flows are almost 2x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low dividend risk.

To conclude, Rockwell Land’s Uniform earnings growth is below among its peers and is trading above with its average peer valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com