Even with the successful adoption of its digital initiatives, this conglomerate’s earnings margin is only at 3%, not 16%

Digital transformation has been an instrumental factor in the improvement of businesses’ processes around the globe, especially during the pandemic

Even before the pandemic, this conglomerate had already established its position in the digital space through the creation of its Digital Transformation Office.

Although as-reported metrics show robust earnings for its impressive innovations, TRUE UAFRS-based (Uniform) earnings reveal that the company has actually recorded less than remarkable results.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Since the late 1980s, digital transformation has been the topic of interest given its instrumentality to society’s continued development.

Adaptation had been gradual, but when the pandemic struck, most businesses had to immediately invest in digital technology.

Manual processes like product sortation and customer support, as well as the building of digital channels to continue operations amid quarantine restrictions, were all automated to some extent.

Even the Philippines’ biggest conglomerates, such as SM Investments (SMP:PHL), Aboitiz Equity Ventures (AEV:PHL), and JG Summit Holdings (JGS:PHL), were not immune to the impact of the pandemic. Just owning generally recession-proof businesses was not enough. Each one had to focus on developing their digital initiatives in order to survive this predicament.

Despite owning one of the largest consumer staples businesses in the country, JG Summit saw its revenues fall by 27% to PHP 221.6 billion in 2020.

Fortunately, the conglomerate has quite a diversified portfolio, holding companies such as Universal Robina Corporation (URC:PHL), Robinsons Land Corporation (RLC:PHL), and Robinsons Retail Holdings (RRHI:PHL) under its belt.

Due to this, JG Summit was able to soften the pandemic’s impact through its strong profits from food, banking, and telecommunications.

One of the factors for this success is the JG Summit’s prioritization of its digital investments.

In 2018, the company had already begun its digital transformation journey through the creation of the Digital Transformation Office (DTO).

To prepare JG Summit’s business units for digitalization, the DTO focused on developing new digital initiatives as well as acquiring the necessary talents with the appropriate skill sets.

In 2019, the DTO unveiled Launchbox, a five-month training program for the company’s business units that would help each unit launch innovative projects, from the discovery phase all the way to product delivery.

Thanks to this concept, JG Summit’s business units were able to develop digital enhancements for their own products and services, namely:

- Universal Robina Corporation’s Sales Force Automation

- Cebu Pacific’s Agility Platform project

- Robinson Land Corporation’s customer services portals

- Robinson Bank’s QuickR feature

At present, the company is further maximizing its digitization efforts with the launch of e-commerce sites for URC’s supermarket and RRHI’s drug store businesses as more people are opting to stay at home because of the pandemic.

Looking at the company’s as-reported metrics, it seems that JG Summit’s early adoption of its digital initiatives helped the company produce generally robust financial data, with margins reaching 16% in 2020 despite pandemic-related headwinds.

In reality, these initiatives were only able to produce margins that never reached more than 60% of as-reported data. In fact, ex-2008, Uniform margins in the past 16 years were the worst in 2020.

What as-reported financials have gotten wrong is the depreciation of the company’s fixed assets.

Depreciation expense is a non-cash expense, meaning it does not represent an actual outlay of cash. As such, depreciation expenses should be added back to earnings. Also, it can be easily manipulated by changing the asset’s life.

However, companies do spend cash on maintenance capital expenditures to ready the same assets for use in the following years. That said, this expense barely shows up in its entirety on the balance sheet.

To arrive at an estimate of the firm’s maintenance capex, what is done instead is smoothing as-reported depreciation expense over a few years, adjusting for inflation and asset impairments.

In JG Summit’s case, PHP 23.9 billion of depreciation expense was charged in 2020, but its substantial growth in assets that year warranted PHP 8.01 billion in maintenance capex.

Along with the many other needed adjustments made, adding back depreciation expense and subtracting maintenance capex leads to just 3% Uniform margins in 2020, lower than its 16% as-reported EBITDA margin.

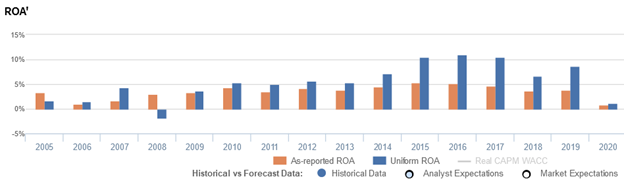

JG Summit’s earning power is generally stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that JG Summit’s profitability has always been at or lower than the cost of capital

In reality, JG Summit’s true profitability has consistently been higher than its as-reported ROA since 2009. For example, as-reported ROA was 5% in 2016, but Uniform ROA is displaying stronger profitability at 11%

Historically, as-reported ROA declined from 3% in 2005 to 1% in 2006, before gradually improving to 5% peaks in 2014-2017 though falling to 1% levels in 2020.

Meanwhile, Uniform ROA gradually expanded from 2% in 2005 to 4% in 2007, before inflecting to negative levels in 2008 and recovering to a high of 11% in 2015-2017. Thereafter, Uniform ROA compressed to 7% in 2018, before improving to 9% in 2019 and declining to 1% in 2020.

JG Summit’s earnings margin is much weaker than you think, but its Uniform asset turns make up for it in recent years

Trends in Uniform ROA have been driven by trends in Uniform earnings margin, and to a lesser extent, Uniform asset turns.

After improving from 4% levels in 2005-2006 to 12% in 2007, Uniform margins inflected negatively in 2008, before recovering to 15% in 2010. Thereafter, Uniform turns contracted to 9% in 2013, before improving to 17% in 2016 and compressing to a low of 3% in 2020.

Meanwhile, Uniform turns sustained 0.4x levels in 2005-2010, before gradually improving to 0.5x-0.7x levels in 2011-2019 and compressing back to 0.4x in 2020.

At current valuations, the market is pricing in expectations for both Uniform margins and Uniform turns to expand.

SUMMARY and JG Summit Holdings, Inc. Tearsheet

As our Uniform Accounting tearsheet for JG Summit Holdings, Inc. (JGS:PHL) highlights, the company trades at a Uniform P/E of 82.8x, above the global corporate average of 23.7x and its median P/E of 16.1x.

High P/Es require high EPS growth to sustain them. In the case of JG Summit, the company has recently shown a 120% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, JG Summit’s sell-side analyst-driven forecast is to see Uniform earnings declines of 222% and 261% in 2021 and 2022, respectively.

The company is currently being valued as if Uniform earnings were to grow 40% annually over the next three years. What sell-side analysts expect for JG Summit’s earnings growth is below what the current stock market valuation requires in 2021 and 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify JG Summit’s PHP 61.00 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power is below the long-run corporate average. Meanwhile, cash flows and cash on hand are also below total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 120bps above the risk free rate. Together, this signals a high dividend and credit risk.

To conclude, JG Summit’s Uniform earnings growth is below its peer averages, but currently trades above its average peer valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers: securities for a living often rely on professionals to manage their own investments within the scope of their investment policies.

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com