Strategic M&As and global partnerships resulted in this company’s 12% Uniform ROA, not below cost of capital!

There are many reasons a company pursues mergers and acquisitions (M&A) in the Telecommunications sector. A few of those reasons are to gain advantage in technology, to expand their customer base, and to diversify their products.

For the past five years, this telecom company has made a number of strategic acquisitions and partnerships that helped it grow. However, as-reported returns do not reflect its success in these initiatives, making the business appear weak. Uniform Accounting shows this company’s REAL profitability.

Also, below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Companies pursue growth in different ways.

A company can grow organically by increasing its productivity and improving its sales without necessarily changing the assets it currently owns.

Said another way, organic growth refers to the growth of the company through its internal operations, relying only on its own resources. To achieve this kind of growth, the company can optimize its processes, reallocate its resources, and add new offerings.

A company can also grow inorganically, meaning through mergers, acquisitions, and takeovers. Compared to organic growth, inorganic growth is a faster way for businesses to expand; however, it is much riskier, as it is greatly affected by a lot of outside factors.

Despite the higher risks, many companies engage in M&A activities as a way to grow. Strategic M&As, if successful, can lead to an expanded market reach, diversified offerings, increase in supply chain pricing power, and may eliminate competition.

In the U.S., among some of the known companies that have expanded its business through successful M&As are Kraft Heinz and Hershey’s in the Consumer Staples industry and Activision Blizzard from the gaming industry.

In the Telecommunications sector, M&As are also very evident and have been a widespread strategy. Given the fast-changing technology, merging and acquiring can broaden a telecom company’s portfolio and expand its services.

Telecom companies especially push through with strategic partnerships in order to acquire new technologies, especially with the increasing trends in 5G, IoT, AI, and other applications.

CITIC Telecom International Holdings Limited is one company in the telecom industry that has taken numerous opportunities to establish itself by enhancing its products and services for its customers through mergers and acquisitions.

In January 2013, the company acquired Companhia de Telecomunicações de Macau (CTM), putting CITIC Telecom in control of Macau’s existing carrier.

In October 2015, CITIC Telecom launched the “CITIC DataMall Global Data Traffic Trading Platform.” To put it simply, CITIC DataMall, the first global data platform of its kind, allows customers to enjoy local data services outside of their country. It is also more convenient since the user doesn’t need to use external devices or buy a new local mobile number.

CITIC DataMall can also lower the costs of accessing international mobile data because it provides flexibility to mobile operators as they can create different packages of mobile data services.

Later that same year, CITIC Telecom entered into a strategic partnership with Symsoft, the operation division of CLX Communications. This partnership was able to combine both companies’ strengths, CLX with its SMS firewall solution and CITIC Telecom with its highly satisfactory services, in order to prevent the occurrence of SMS spam and fraud.

The company also fully acquired Linx Telecommunications in February 2017 to further achieve its expansion goals. This acquisition enabled CITIC Telecom to be one of the lead ICT service providers in Asia.

It also helped the company become a global service provider as it was able to tap into 14 more countries serviced by the enterprise acquired, enabling the quickened expansion of the operations of its cloud and data center.

Moreover, in light of the different technological developments such as IoT, AI, and cloud computing, CITIC Telecom entered into another strategic cooperation framework agreement with China Mobile International Limited this year.

These acquisitions and joint ventures helped CITIC Telecom expand globally and improve its offerings, giving it the opportunity to reach a larger consumer base and improve its profitability.

However, this is not translated in the company’s as-reported ROAs. In recent years, the company has below cost-of-capital as-reported returns, making it appear like it hasn’t really benefited from its strategic M&As and partnerships.

Uniform Accounting tells us otherwise, showing more robust returns for CITIC Telecom. Currently, its Uniform ROA sits at 12%, thanks to its strategic partnerships and acquisitions.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on CITIC Telecom’s balance sheet. The company’s goodwill currently sits at about HKD 9.7 billion due to the aforementioned acquisitions plus its other acquisitions over the course of its operations.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the true strength of CITIC Telecom’s profitability. After adjusting for goodwill and all other necessary adjustments, we can see that the company isn’t actually displaying a weak, below cost-of-capital performance. In reality, for the past sixteen years, Uniform ROAs are consistently more robust than what as-reported metrics show.

CITIC Telecom International’s profitability is more robust than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

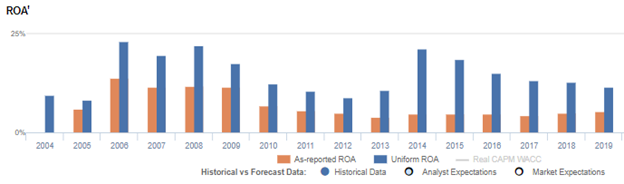

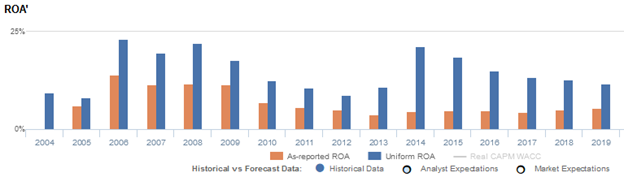

CITIC Telecom’s Uniform ROA has been higher than its as-reported ROA in the past sixteen years. For example, when Uniform ROA peaked at 23% in 2006, as-reported ROA was only 14%.

The company’s Uniform ROA for the past fifteen years has ranged from 8% to 23%, while as-reported ROA remained only between 4% and 14% in the same time frame.

From 8%-9% levels in 2004-2005, Uniform ROA reached a peak of 23% in 2006 before declining back to 9% in 2012. Uniform ROA then jumped to 21% in 2014 before gradually decreasing to 12% in 2019.

CITIC Telecom International’s Uniform earnings margins are weaker than you think, but its Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform asset turns and to a lesser extent, Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

After rising from 9% in 2004 to 15% in 2009, Uniform margins compressed to 10%-11% levels from 2010-2013 before elevating to 15%-18% levels through 2019.

Uniform turns rose from 0.9x in 2005 to a peak of 1.8x in 2006. It then fell to 0.9x levels in 2012-2013 before jumping to 1.3x in 2014 and fading to 0.8x levels in 2018-2019.

SUMMARY and CITIC Telecom International Holdings Limited Tearsheet

As the Uniform Accounting tearsheet for CITIC Telecom International Holdings Limited (1883:HKG) highlights, its Uniform P/E trades at 13.0x, which is below corporate average valuation levels and around its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of CITIC Telecom, the company has recently shown an 11% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Hong Kong Financial Reporting Standards (HKFRS) earnings and convert them to Uniform earnings forecasts. When we do this, CITIC Telecom’s sell-side analyst-driven forecast is 15% and 9% earnings growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify CITIC Telecom’s HKD 2.45 stock price. These are often referred to as market embedded expectations.

CITIC Telecom can have a 6% Uniform earnings shrinkage for each of the next three years and still justify current market expectations. What sell-side analysts expect for CITIC Telecom’s earnings is above what the current stock market valuation requires in 2020 and 2021.

The company’s earning power is 2x the corporate average. However, cash flows and cash on hand are slightly below its total obligations. Together, this signals a moderate credit and dividend risk.

To conclude, CITIC Telecom’s Uniform earnings growth is below its peer averages in 2020, and the company is trading well below its peer valuations.

About the Philippine Markets Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com