This holding company banked on a Uniform ROA that is more robust than its as-reported

It’s pretty common for businesses to be named after their owners. Whether the names are in the form of initials, surnames, or full names, owners do this as a sign of the fruits of their labor or to create a legacy that will be remembered after they are gone.

One business owner, in particular, was able to transform a bank into one of the largest business conglomerates in the Philippines with diverse exposure to numerous industries. Based on its historical Uniform ROA, this conglomerate shows that through diversification, it was able to record more robust profitability than analysts might think.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In the Philippines, some of the names of the largest conglomerates are affiliated with their most notable founding members. We have Lucio Tan with LT Group, Inc. (LTG:PHL), John L. Gokongwei, Jr with JG Summit Holdings (JGS:PHL), and Manuel Villar with Golden MV Holdings, Inc. (HVN:PHL).

Today, we will talk about another conglomerate named after its founder who began his massive portfolio of businesses through banking.

In the 1960s, an immigrant from Hong Kong established Metrobank as a means to specifically provide financial services to the Filipino-Chinese community.

As a company, Metrobank strived for diversification in its services in order to give a broad range of products and services to its customers.

This eventually led to the diversification of its businesses by venturing with internationally recognized companies such as Toyota Motor and AXA Group. Because of this, the Metrobank group enhanced its growth potential with exposure in the automotive and life insurance industries, respectively.

Named after the late George S. K. Ty, GT Capital Holdings, Inc. (GTCAP:PHL) was incorporated in 2007 and was publicly listed in 2012. Along with Metrobank, the interests of the group’s ventures and businesses were consolidated into the non-bank holding company.

As a result, GT Capital currently has shares in the aforementioned industries, including the banking industry. The conglomerate has interests as well in the following sectors: Property Development (Federal Land), Power Generation (Global Business Power), Nonlife Insurance (Charter Ping An Insurance), Infrastructure and Utilities (Metro Pacific Investments Corporation), and Motorcycle Financing (Sumisho Motor Finance Corporation).

However, expansion through exposure to multiple industries has its risks, especially when the affected industry is one of its largest components.

In 2020, GT Capital’s net income dropped by 67% due to weakness in its automotive operations segment. Comprising 87% of GT Capital’s revenue in 2020, the segment was severely impacted by the Taal eruption and the community quarantine restrictions as vehicle demand declined that year.

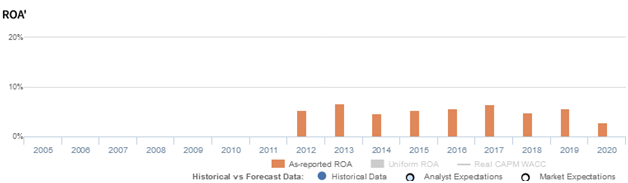

Looking at the as-reported metrics, GT Capital’s sales continued to produce returns near cost-of-capital levels, implying that the conglomerate has generated little economic value for its stockholders since 2012.

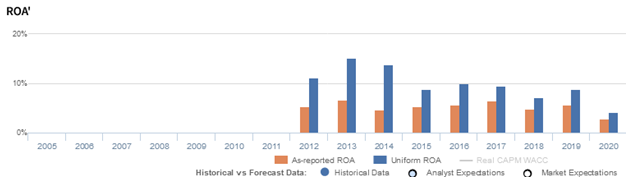

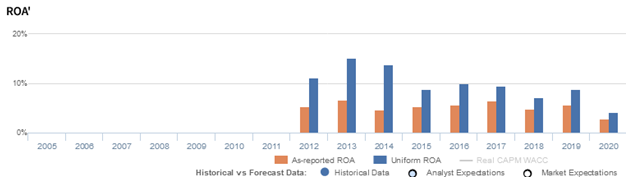

However, Uniform Accounting tells us that GT Capital’s profitability is more robust than what the as-reported figures show.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of non-operating long-term investments on GT Capital’s balance sheet.

These long-term investments are intangible assets that are purely accounting-based and unrepresentative of the conglomerate’s actual operating performance. When as-reported accounting includes this in a conglomerate’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of GT Capital’s earning power. When non-operating long-term investments are adjusted from the conglomerate’s assets, along with the many other necessary adjustments made, this leads to a 4% Uniform ROA in 2020.

GT Capital’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think GT Capital’s profitability has been weaker than real economic metrics have highlighted.

In reality, GT Capital’s true profitability has been higher than as-reported ROA in the past nine years.

After rising from 11% in 2012 to a peak of 15% in 2013, Uniform ROA gradually declined to 4% in 2020. In contrast, after ranging from 5% to 7% levels in 2012-2019, as-reported ROA faded to a low of 3% in 2020.

GT Capital’s asset turns are more efficient than you think

Similarly, as-reported metrics significantly distort the firm’s asset efficiency, a key driver of profitability.

Since 2012, as-reported ROA has never exceeded 0.9x, while Uniform ROA has reached a peak of 1.1x in 2014, substantially distorting the market’s perception of GT Capital’s historical asset efficiency level.

SUMMARY and GT Capital Holdings, Inc. Tearsheet

As our Uniform Accounting tearsheet for GT Capital Holdings, Inc. (GTCAP:PHL) highlights, the company trades at a Uniform P/E of 3.9x, below the global corporate average of 24.0x, and its historical P/E of 6.2x.

Low P/Es require low EPS growth to sustain them. In the case of GT Capital, the company has recently shown a 68% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, GT Capital’s sell-side analyst-driven forecast is to see Uniform earnings growth by 125% and 39% by 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify GT Capital’s PHP 567.00 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 26% annually over the next three years. What sell-side analysts expect for GT Capital’s earnings growth is well above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is below the long-run corporate average. Moreover, cash flows and cash on hand are below total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a moderate dividend and credit risk.

To conclude, GT Capital’s Uniform earnings growth is in line with its peer averages, and currently trades above its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com