This liquor company was able to fix itself to become a heritage brand in China, with Uniform ROAs 36x the as-reported

Diageo used to be the world’s biggest liquor company by value until a Chinese distiller came along with nearly half a trillion dollars in market capitalization. This distiller takes its place as the most valuable non-tech company in China despite being relatively unknown in most parts of the world.

Uniform Accounting reveals that the company has actually had more robust profitability for the past sixteen years than what as-reported metrics show.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

There are only a handful of brands that have become so ingrained in our daily lives that we are unable to imagine life without them. Nearly everywhere we look, we can see these brands’ products either on ads or being consumed.

For example, we see Coca-Cola products being set up in football conferences, interviews, business events, and political banquets. Its mainstream media penetration has come to a point wherein we no longer question it and instead embrace these product placements as they are.

Kweichow Moutai is no different. Its liquor, Moutai baijiu, is likened to Coca-Cola’s sodas as a heritage brand in China. In fact, its market cap exceeds that of Coca-Cola’s as well as other formidable companies such as Starbucks, Suntory, and Heineken.

Now the most prominent question that comes to mind is how this Chinese company managed to achieve its $421 billion market value.

Kweichow Moutai Co. attracts a vast number of investors primarily due to its financial stability given how much of a staple its products have become.

The brand’s popularity, specifically its Moutai baijiu, stems from its historical presence. It is often dubbed as Mao Zedong’s favorite liquor; the liquor even has tales of being used as Chinese soldiers’ disinfectant and anesthesia during the Red Army’s “Long March.”

As the name suggests, Moutai can only be produced in one specific area, in the quaint town of Maotai located in Guizhou province. Its climate and local river are integral in giving Moutai its unique notes.

Thanks to this unique production process and Moutai’s rich history, the company is able to generate sufficient demand for its expensive products, which are linked to one’s wealth and social status.

Over the course of the COVID-19 pandemic, Moutai baijiu sales have grown stronger pushing its stock price to surge by more than 60%. The strict regulations imposed on travelers have led locals to shift their focus on tangible commodities, splurging on luxury items such as Moutai baijiu.

In this sense, the pandemic has given the company even more leverage to sell its products at a premium due to the higher demand.

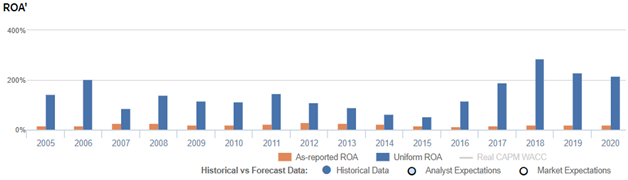

As-reported metrics show that the company may be just moderately profitable despite its success, with as-reported ROAs trending at 15%-29% from 2005 to 2020.

However, this does not fully capture the company’s real profitability. Under a Uniform Accounting perspective, the company is actually generating much more impressive profits.

For the past sixteen years, the company’s Uniform ROA has actually ranged from 53% to 285%.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

When excess cash remains included in the company’s asset base while computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is.

Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

From 2012 to 2020, Kweichow Moutai has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 40% to 67% of its as-reported total assets.

After excess cash and other necessary adjustments are made, we can see that Kweichow Moutai’s current returns are actually a lot stronger than what as-reported metrics show. Without these adjustments, it appears that the company’s innovative efforts are not translating into profitability, leading to significantly poorer valuations.

Kweichow’s profitability is much more robust than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics reveal.

Kweichow’s Uniform ROA has been higher than its as-reported ROA for the past sixteen years. For example, when Uniform ROA was at 218% in 2020, as-reported ROA was only 20%.

The company’s Uniform ROA for the past sixteen years has ranged from 53% to 285%, while as-reported ROA has ranged only from 15% to 29% in the same timeframe.

Specifically, Uniform ROA jumped from 144% in 2005 to 205% in 2006, before dropping to 88% in 2007. It then remained at 114%-147% levels from 2008 to 2011, before declining to 53% in 2015. Uniform ROA then peaked at 285% in 2018 before contracting to 218% in 2020.

Kweichow’s Uniform earnings margins are weaker than you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in both Uniform earnings margin and Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

After gradually rising from 30% in 2005 to 53% in 2012, Uniform margins dropped to 43% in 2016. Uniform margins then recovered to 49% in 2020.

Meanwhile, Uniform turns jumped from 4.7x in 2005 to 6.0x in 2006 before gradually declining to 1.1x in 2015. It then peaked at 6.1x in 2018, which eventually contracted to 4.5x in 2020.

SUMMARY and Kweichow Moutai Co., Ltd. Tearsheet

As the Uniform Accounting tearsheet for Kweichow Moutai Co., Ltd. (600519:CHN) highlights, its Uniform P/E trades at 34.0x, which is above the global corporate average of 23.7x and its own historical average of 31.1x.

High P/Es require high EPS growth to sustain them. In the case of Kweichow Moutai, the company has recently shown a 15% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Chinese Accounting Standards (CAS) earnings and convert them to Uniform earnings forecasts. When we do this, Kweichow Moutai’s sell-side analyst-driven forecast is a 15% and 20% earnings growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Kweichow Moutai’s CNY 1,700 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 17% annually over the next three years. What sell-side analysts expect for Kweichow Moutai’s earnings is below with the current stock market valuation required in 2021 but above that requirement in 2022.

Furthermore, the company’s earning power is 36x above the long-run corporate average. Also, cash flows and cash on hand are almost 8x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, Kweichow Moutai’s Uniform earnings growth is below its peer averages. However, the company is trading in line with its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com