Uniform Accounting shows how this conglomerate has been holding companies with more than double 4% as-reported returns

Over the recent weeks, the possibility of a “Big Bath” scenario occurring anywhere in the world has been discussed. It could happen in the United States’ airline industry, China’s real estate sector, or the Philippines’ largest fast food chain.

It can also occur in one of the Philippines’ largest conglomerates, affirming that this accounting issue can occur in any industry and anywhere in the world.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Goodwill is one of the more common and largest distortions found in the financial statements of many companies around the world. It is essentially the premium that a company pays to acquire another company.

As such, companies that have a history of acquiring many businesses often hold a significant amount of goodwill.

While goodwill recognition is required by GAAP and IFRS to satisfy the matching principle, it is purely accounting-based and is not representative of the company’s actual operating performance.

In addition, goodwill is often charged with impairment losses and gains, thereby affecting the income statement as well. This opens up a scenario where management can make their firm’s performance in a quarter weaker than it truly is, especially during economically difficult quarters.

That event is known as the “Big Bath,” which Valens Research President and CEO Litman discussed in his latest Forbes article.

A Big Bath scenario occurs when a collapse in actual cash earnings is compounded by a financial reporting anomaly.

With the COVID-19 pandemic hampering business for the entire second quarter, it is likely that companies will pile expenses such as goodwill impairments to depress further an already unrecoverable quarter. By doing so, they can make themselves appear to be outperforming in the succeeding quarters.

We have seen a Big Bath event before in Aboitiz Equity Ventures (AEV:PHL). The conglomerate has made numerous acquisitions in the past to supports its diversified stakes in:

- The power generation industry through Aboitiz Power (AP:PHL)

- The food manufacturing industry through the Pilmico brand, and

- The real estate sector through AboitizLand

For this reason, the company has accrued a lot of goodwill over the years. Amidst the 2008 Global Financial Crisis, the company recognized a PHP 560 million impairment loss and reported only PHP 745 million net earnings in Q4 2008, a 36% decline from the previous quarter.

Immediately after, the company reversed the impairment loss in Q1 2009. The firm reported a PHP 1.42 billion profit and misled investors to think that it doubled its earnings quarter-over-quarter.

Besides the goodwill distortion, the Philippine Financial Reporting Standards (PFRS) permits companies to measure financial assets based on their fair value. In times of economic uncertainty, the fair value of assets can fluctuate wildly from quarter to quarter and can result in massive gains or losses.

In the case of conglomerates such as Aboitiz Equity, their cash is often held in the form of financial assets, which are measured based on their fair value.

With the Philippines’ own stock market sell-off last March, Aboitiz Equity was required to recognize an unrealized mark-to-market loss of PHP 117.8 million. With Q1 2020 as-reported earnings already falling 40% year-over-year, the unrealized loss depresses earnings further.

In reality, Aboitiz Equity’s earnings have been more robust than what as-reported financials imply. Since the company’s acquisition of various power plants in 2009, the disparity between the company’s Uniform earnings power and as-reported ROA has widened.

Besides the unusual item adjustment on the earnings side, Aboitiz Equity’s non-operating long-term investments must also be adjusted on the assets side.

Composed mostly of long-term financial securities and non-controlling ownership interests, these are not considered to be core to the company’s operations since the firm has no management influence on either of these.

As such, removing non-operating long-term investments from the balance sheet and with the other adjustments Valens makes, Aboitiz Equity’s Uniform earning power has actually been more than 2x as-reported ROA since 2014.

Aboitiz’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

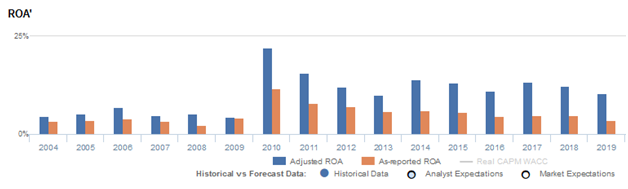

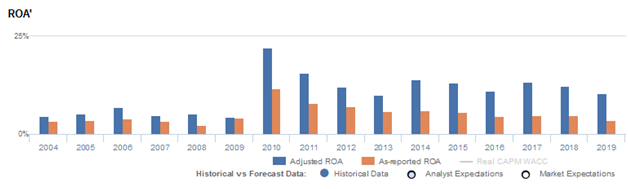

Through Uniform Accounting, we can see that the company’s true ROAs have actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 4% in 2019, but its Uniform ROA was actually higher at 10%.

From 2004 to 2006, Uniform ROA improved from 5% to 7% levels before declining to its lowest level of 4% in 2009. Then, Uniform ROA peaked at 22% in 2010 following the company’s acquisition of 747 Megawatt (MW) Tiwi-MakBan Geothermal Power Plant, before collapsing to 10% in 2013. Thereafter, Uniform ROA ranged from 11%-14% in 2014-2018, before deteriorating back to 10% levels through 2019.

Aboitiz is a more efficient business than you think

Aboitiz’s strong profitability has been primarily driven by robust asset turns.

Uniform asset turns had steadily increased in 2004-2007, ranging from 1.1x-1.5x, before dropping to 0.5x in 2009. Then from 2010-2015, Uniform turns had improved, ranging from 0.7x to 0.9x, before fading back again to 0.5x in 2016. Thereafter, Uniform asset turns improved to 0.7x in 2019.

At current valuations, markets are pricing in expectation for stability in Uniform asset turns and Uniform earnings margin.

SUMMARY and Aboitiz Equity Ventures, Inc. Tearsheet

As the Uniform Accounting tearsheet for Aboitiz highlights, the Uniform P/E trades at 18.2x, which is below corporate average valuation levels but around its own history.

Low P/Es require low EPS growth to sustain them. In the case of Aboitiz, the company has recently shown a 17% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Aboitiz’s sell-side analyst-driven forecast calls for 13% Uniform EPS decline in 2020, followed by a 12% Uniform EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Aboitiz’s PHP 47.00 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 6% each year over the next three years and still justify current prices. What sell-side analysts expect for Aboitiz’s earnings growth is far below what the current stock market valuation requires.

The company’s earning power is 2x the long-run corporate average. However, cash flows will fall short of its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals moderate credit and high dividend risk.

To conclude, Aboitiz’s Uniform earnings growth is below peers in 2020, and the company is trading below peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com