Uniform Accounting unveils that this company doesn’t just build affordable homes, but it also develops 2x as-reported returns

In our past Tuesday articles, we talked about the rags-to-riches stories of Filipino tycoons like Henry Sy and John Gokongwei, Jr.

The next tycoon we’re highlighting is known for his interest in a variety of businesses. Most people might know him because of his subdivision developments, but his largest public company might come as a surprise, particularly once you learn how it started.

This company’s performance looks modest and stagnant according to its as-reported financials. However, when looking at the company through Uniform metrics, that company has actually been getting livelier.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Death is a deeply personal topic. While many shy away from talking about it, Manuel “Manny” Villar saw what others didn’t — a promising business opportunity within an industry full of practices and traditions.

Manny Villar founded Golden Haven, Inc. in 1982 to meet the underserved demand of the death care industry.

Although more recognized through his businesses Starmalls and Vista Land, it was Villar’s ownership of Golden Haven that propelled him to become the Philippines’ richest man in 2019, taking the spot of the late Henry Sy, Sr.

Like the previous tycoons we talked about, Villar was not born with a silver spoon.

Villar’s entrepreneurial history could be traced back to 1975, when he borrowed PHP 10,000 to buy two reconditioned trucks to haul gravel and sand for construction companies in Las Piñas.

Later on, he managed to purchase a number of lots in Las Piñas by applying for an additional bank loan. He then turned his focus to providing low-cost housing and the eventual founding of Vista Land and Lifescapes (VLL:PHL).

In 1982, Manny Villar established Golden Haven, Inc. (HVN:PHL) to build memorial lots and columbariums across the country. He thought his home development experience could be easily applied to the budding death care market.

For most of Golden Haven’s existence, the company represented a small portion of Villar’s wealth. It was only in 2016 when it began to rapidly grow, debuting in the Philippine Stock Exchange in the same year.

To attract hesitant investors, Golden Haven diversified its business and acquired mass housing developer Bria Homes. Golden Haven rebranded itself to Golden Bria Holdings, Inc. to allow more flexibility in real estate development, while still maintaining its death care business.

Thanks to its acquisition, Golden Bria saw its stock surge by more than 1,300%. From PHP 22.00 in January 2018, the firm’s stock price is now hovering around PHP 309.00 per share.

The company’s stock performance drove its market capitalization to more than PHP 200 billion, surpassing Manny Villar’s other businesses and becoming his largest public holding.

Uniform Accounting reflected what the market saw. Golden Bria was already profitable before the Bria Homes acquisition, but it still saw returns double after the acquisition.

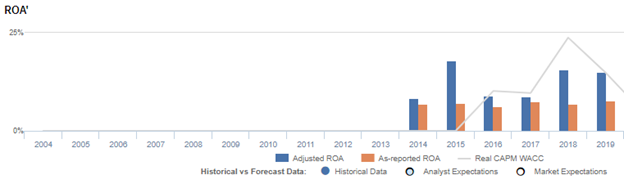

As-reported metrics suggest that the company’s ROA in 2018-2019 ranged only from 7%-8%, whereas using Uniform accounting, ROA is actually 2x as-reported figures at 15%-16%.

One of the main reasons for the disparity stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

Based on PFRS, interest expense is an operating cash flow, but in reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

In 2019 alone, Golden Bria recognized an interest expense of PHP 258 million. When we add the PHP 258 million back to earnings because it is not an operating expense, net income increases.

By applying this adjustment together with other necessary adjustments that Valens makes, we arrive at the company’s TRUE earning power of 15%.

Golden Bria’s earning power is stronger than you think

Through Uniform Accounting, we see that as-reported metrics significantly distort the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than what real economic metrics reveal.

Uniform ROA has actually been higher than as-reported ROA for the past six years. In 2019, Uniform ROA was 15%, which is almost twice its as-reported ROA of 8%.

After improving from 8% in 2014 to a peak level of 18% in 2015, Uniform ROA declined to 9% in 2016-2017. It then improved once again to 15%-16% levels in 2018-2019 after the firm’s acquisition of Bria Homes.

Meanwhile, as-reported ROA only improved from 6%-7% in 2014-2016 to 8% in 2017-2019.

Golden Bria is a more efficient business that you think

Trends in Uniform ROA have largely been driven by similar trends in Uniform asset turns, suggesting that the firm has relied more on efficient asset utilization for earnings growth.

From 2014 to 2015, Uniform asset turns improved from 0.4x to an all time high of 0.8x, before declining back to 0.4x in 2016. Uniform turns then reached 0.6x levels in 2018, before deteriorating to 0.5x in 2019.

In every year, as-reported metrics have understated the company’s true asset turns, making the company appear to be less efficient in the use of assets than real economic metrics highlight.

SUMMARY and Golden Bria Holdings Inc. Tearsheet

As the Uniform Accounting tearsheet for Golden Bria highlights, the Uniform P/E trades at 73.8x, which is far above corporate average valuation levels and its own history.

High P/Es require high EPS growth to sustain them. In the case of Golden Bria, the company has recently shown a 64% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Golden Bria’s sell-side analyst-driven forecast calls for a 1% Uniform EPS deterioration in 2020 followed by immaterial Uniform EPS decline in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Golden Bria’s PHP 305.00 stock price. These are often referred to as market embedded expectations.

To justify current valuation, the company would need to grow its Uniform earnings by 43% each year over the next three years. What sell-side analysts expect for Golden Bria’s earnings growth is far below what the current stock market valuation requires.

The company’s earning power is 2x the long-run corporate average. In addition, cash flows and cash on hand are significantly above its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Golden Bria’s Uniform earnings growth is above peer averages in 2020, and the company is trading below peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com