Affordable housing shaped this property behemoth’s whole portfolio, building a Uniform ROA of 6%, not 4%

Expensive housing and overpopulation in cities have been considered as two of the most pressing issues in the Philippines, resulting in affordable housing being more in demand as it has ever been.

This property behemoth made it its mission to build and diversify its property portfolio to be able to cater to all income segments. However, looking at its as-reported metrics, it seems that mainly focusing on this core strategy hasn’t been enough to achieve above cost-of-capital returns.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In his article Economic Development and the Housing Problem, William J. Keyes stated that “developing countries, generally, over the past few decades have not given adequate attention to their housing problem, presumably because of more pressing economic needs.”

Until now, this statement holds true in the Philippines given that the country still faces the same problems of housing costs amid a rapidly increasing population, with a majority of Filipinos unable to earn enough income to cover more than the basic necessities.

Vista Land & Lifescapes, Inc. (VLL:PHL) took this as an opportunity and made it the company’s mission to build different kinds of properties that would cater to all income segments across the country. It operates through its five subsidiaries, namely, Brittany, Crown Asia, Camella Homes, Communities Philippines, and Vista Residences.

Throughout the years, the company stuck to its core strategy of continuously building homes for the Filipino people. Its flagship brand, Camella, caters to the middle-income segment and started out as only one property in Las Piñas. Now, it has already built around 500,000 homes across 47 provinces and 149 cities.

Furthermore, much like Megaworld’s township developments, Vista Land also focused on developing its “communicities,” which combine essential and non-essential forms of establishments into one location. These include lifestyle retail, prime office spaces, university towns, healthcare, and other leisure components.

However, operating in the real estate industry is more than just your regular DIY project. For starters, having big competitors, such as Ayala Land and SM Prime, is already in and of itself a challenging feat to overcome.

In order to do well in the industry, Vista Land expanded its scope outside its competitors’ market reach by launching some of its projects in “second-tier” cities in 2013, including Zambales, Kalibo, and Roxas. As a result, Vista Land now has the widest geographic presence in the country among all homebuilders.

In 2015, Vista Land also ventured into the retail and commercial segment by acquiring mall and office developer Starmalls Incorporated for P33.5 billion to further diversify its portfolio.

With both being owned by the Villar Group, securing this transaction further enabled Vista Land to speed up the rollout of its development projects while opening its doors to potential partnerships with other real estate developers, which further solidified its position in the industry.

Currently, its commercial arm operates around 101 commercial assets, which comprises 31 malls, 63 commercial centers, and seven BPO office spaces.

Overall, being one of the largest homebuilders in the country has its advantages. Vista Land’s diversified property portfolio has allowed it to easily carry out its expansion and development plans and expansion initiatives.

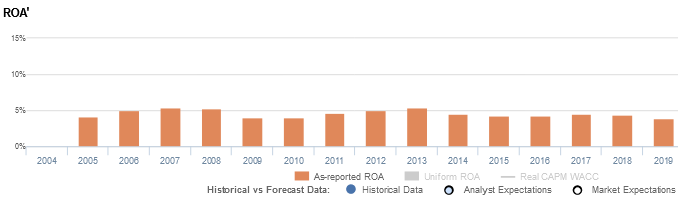

However, as-reported metrics don’t show that Vista Land is the successful property behemoth that it is—with return on assets (ROAs) barely surpassing cost-of-capital levels over the past sixteen years.

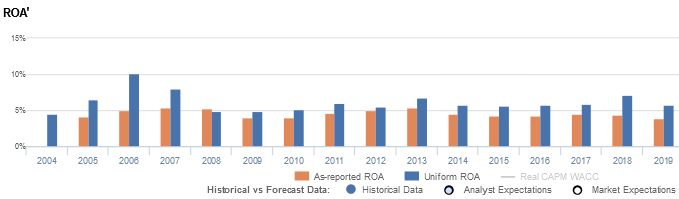

In reality, its diverse property portfolio consisting of houses, condominiums, and malls, and investments in their expansion initiatives have led to better Uniform returns of more than 6%.

One of the said distortions for the discrepancy is due to the treatment of non-operating long-term investments according to the Philippine Financial Reporting Standards (PFRS).

Based on PFRS, non-operating long-term investments are part of the company’s balance sheet, but in reality, non-operating long-term investments are not essential to the firm’s assets and should be removed from the total assets.

For example, in 2019, Vista Land recognized a non-operating long-term investment of PHP 32.3 billion, accounting for 12% of its as-reported total assets of PHP 272.5 billion.

After removing the PHP 32.3 billion item from the asset base and with the many other necessary adjustments Valens makes, we arrive at a TRUE earning power of 6%.

Vista Land’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think Vista Land’s profitability has been weaker than real economic metrics have highlighted in fifteen of the past sixteen years.

In reality, Vista Land’s true profitability has generally been higher than as-reported ROA since 2005. Specifically, Uniform ROA was 6% in 2019, but as-reported ROA was only 4% that year. Though this difference may seem small, it’s actually the difference between a profitable company and a company barely earning enough to cover its cost of capital.

Since 2005, as-reported ROA has ranged from 4%-5% levels through 2019, and is currently sitting at the lower end of that range.

Meanwhile, after expanding from 7% in 2005 to a peak of 10% in 2006, Uniform ROA declined to 5% levels in 2008-2010, before improving to 6%-7% levels through 2019.

Vista Land’s earnings margin is weaker than you think

Trends in Uniform ROA have been primarily driven by trends in Uniform earnings margin.

As-reported margins improved from 26% in 2004 to 35%-36% levels in 2005-2008, before fading to 32%-34% levels in 2009-2014 and subsequently recovering to 41%-42% levels in 2017-2019.

Meanwhile, Uniform margins expanded from 19% in 2004 to 34% in 2006, before compressing to 27% levels in 2008 and rebounding to 30% levels in 2017-2018. Since then, Uniform margins have regressed to 28% in 2019.

Looking at the firm’s margins alone, as-reported metrics are making the firm appear to be a more cost efficient business than is accurate.

SUMMARY and Vista Land & Lifescapes, Inc. Tearsheet

As the Uniform Accounting tearsheet for Vista Land & Lifescapes, Inc. (VLL:PHL) highlights, it trades at a Uniform P/E of 19.1x, below the global corporate average of 25.2x, but around its historical average of 17.6x.

Low P/Es require low EPS growth to sustain them. In the case of Vista Land, the company has recently shown a 1% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Vista Land’s sell-side analyst-driven forecast calls for a 56% Uniform EPS decline in 2020 and a 30% Uniform EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Vista Land’s PHP 3.80 stock price. These are often referred to as market embedded expectations.

Vista Land is currently being valued as if Uniform earnings were to shrink 5% annually over the next three years. What sell-side analysts expect for Vista Land’s earnings growth is below what the current stock market valuation requires in 2020 but above the requirement in 2021.

Furthermore, the company’s earning power is near the long-run corporate average, and cash flows and cash on hand are also above total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low dividend risk.

To conclude, Vista Land’s Uniform earnings growth is below its peer averages, but the company is trading in line with its peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com