MONDAY MACRO: Uniform Accounting tells us despite the gloom in 2020, we shouldn’t expect doom for the Philippine economy in 2021

2020 will likely go down in history as one of the most challenging years globally for health care, economies, and even the stock market.

The Philippine stock market, in particular, faced pressures as early as January when the Taal Volcano erupted. Then, in March, the COVID-19 community quarantines nearly brought the local stock market to its decade lows, touching 4,000 levels. Though the market has since recovered, it has yet to return to its 7,500+ level at the start of the year.

As 2020 comes to a close, we take a look at how the Philippine economy fared by understanding the various economic indicators through Uniform Accounting lenses.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

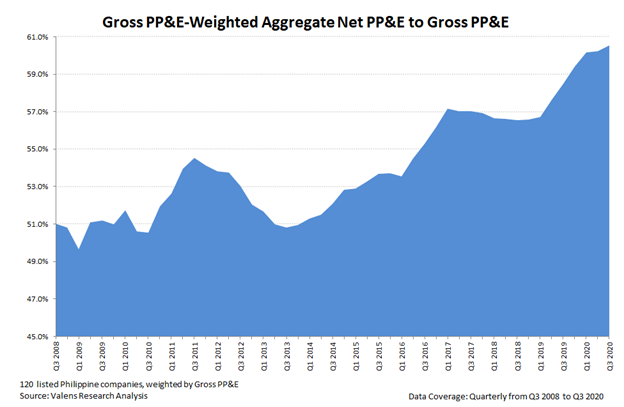

Net/Gross PP&E slightly improves

One of our indicators for economic growth is capacity utilization, which determines the potential output of companies realized without additional capex spending.

Companies operating at 85% capacity utilization are normally considered as operating at an optimal rate. A value above 85% means corporations need significant capex spending to grow, which could cause inflation.

Large dips in capacity utilization are a lagging indicator of a recession. They signal that capex will likely be subdued going forward, and is also a signal of lower inflation going forward, due to slack in the economy.

Although capacity utilization had improved to 67% in September-October, above its low of 65% in August, it is still far below ideal levels.

However, it is important to remember this decline in capacity utilization is different from previous declines. Physical distancing and quarantine measures have pressured this metric, not structural problems in the wider economy.

This means that as the quarantine restrictions are eased, capacity utilization could rebound way faster than it normally does, assuming there aren’t other follow-on issues.

This is why capacity utilization is analyzed in tandem with another growth indicator, the Net/Gross PP&E ratio, which reveals that firms are still spending on capex as of Q3 2020. At around 61%, this ratio indicates that firms remain more focused on widening their growth prospects, expanding their production capacities, or developing ways to prevent infections while working.

Uniform ROA declines for now

Similar to the capacity utilization, implemented community quarantines have negatively affected corporate profitability by 33% in 2020 from PHP 700 billion to an expected PHP 468 billion. Because of this, Uniform ROA is expected to decline to 5%.

In addition, revenue generation will continue to be challenged by a lack of consumer confidence, which has been essential for consumer demand and business profitability. With a record-low of -54.5%, the country is showing weak signals for consumer demand.

However, with accommodative fiscal measures from the government such as relief funds for businesses and vaccine availability by next year, the rebound in profitability to near pre-coronavirus levels of 6% by 2021 is warranted.

Interest Expenses have less coverage

With the declining corporate profitability comes the weakening of the current aggregate interest coverage ratio, a metric that shows firms’ current ability to cover their financial obligations when no momentary relief is granted to them.

Calculating this ratio with the earnings before interest, taxes, amortization, and pension (EBITAP) as a numerator serves as a measurement to determine a firm’s solvency. Even at its lowest in the last decade at 2.5x, firms in aggregate still have the capacity to pay their interests. Thus, signifying their ability to service their loans without defaulting.

An interest coverage ratio of 1x means that a company is generating the same amount of earnings before interest, taxes, amortization, and pension (EBITAP) to service its interest expense.

Generally, investors require companies to have at least 2x interest coverage ratio. Generating EBITAP that’s double the short-term financial obligations gives investors assurance that the company still has the resources to fund its growth.

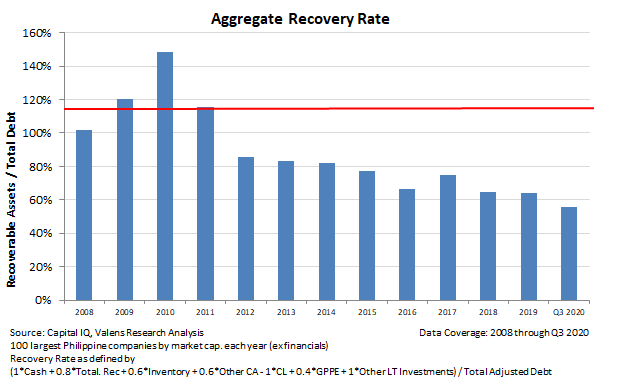

Recovery Rates are down, though not yet that big of a concern

We mentioned in our previous Monday Macro on aggregate recovery rate, that the all-time decline of 56% was caused by the contraction of firms’ recoverable assets outpacing total debt contraction. With limited alternatives because of the pandemic, companies are expected to turn to debt to survive.

The declining asset quality is something to be concerned about because of credit risk concerns that may arise from it, especially if interest rates remain high. Fortunately, the Bangko Sentral ng Pilipinas (BSP) has been one of the most aggressive central banks in the world in terms of rate cuts. It has been actively adjusting its monetary policies to aid the country’s economic recovery.

The BSP also still has the reserve requirement ratio (RRR) of 12% in its arsenal. Banks are currently required to hold a minimum of 12% of deposits that cannot be loaned out. This is still a conservative rate, higher than neighboring countries’ single-digit rates. The BSP can still choose to adjust this rate lower to entice banks to increase their lending activities.

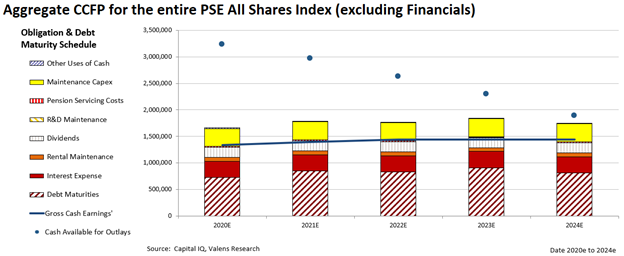

Credit fundamentals remain healthy

The updated financial results for Q3 2020 reveal that credit fundamentals should help ease concerns about disruptions in the economy. Using the aggregate Credit Cash Flow Prime (CCFP), we see that Philippine firms’ operating and debt obligations can be paid by their cash buffers and cash flows for the next five years.

Looking at all these indicators, we see that although investors have reason to be concerned about the Philippine economy in the near term, their concerns about a credit crunch are overstated. Accommodative monetary policies from the central bank, the sizable liquidity that firms have, a robust financial system, and the low risks of increasing credit defaults from corporations all show that the Philippines will be able to bounce back quickly once the pandemic ends.

However, weak consumer demand and tight credit standards will become headwinds to the availability of capital for firms in the near term. Furthermore, other corporate fundamentals provide pessimistic signals for credit risk as aggregate earnings and asset quality gradually decline, which limits the chances of firms to serve their financial obligations.

Overall, because this recession was not credit-driven and since the contraction was caused by government-mandated shutdowns and quarantines, we expect to see a pickup in business activities and a quicker recovery in the next year.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com