Taking advantage of the growing real estate market has led this company to show 6% Uniform ROA, not below cost of capital per as-reported metrics

Prior to the pandemic, the real estate industry was one of the fastest growing and attractive spaces in the Philippines. As the country grew, so did expansion projects for urbanization, as well as residential and office spaces because of growth in the BPO sector.

These are some of the reasons why this real estate developer was able to generate strong returns. However, as-reported metrics are consistently showing weaker profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

A year ago, Wuhan closed its city to keep the coronavirus from spreading, and other Chinese cities followed suit. China was in lockdown, and months later, so was the rest of the world.

The restrictions placed on travel and business activities caused many investors to panic, leading to global market sell-offs. Retailers, restaurants, and entertainment spaces were some of the hardest hit industries as people stayed at home to avoid contracting the virus, and one sector was in the middle of it all.

The real estate industry includes residential, office, and shopping spaces, among others. With tenants closing and offices shifting to work-from-home setups, the sector’s income source seemed to be depleting.

We discussed how these top real estate developers, Ayala Land Inc. (ALI:PHL) and SM Prime Holdings, Inc. (SMPH:PHL) have been affected.

Today, we will cover another successful property developer Robinsons Land Corporation (RLC:PHL).

Robinsons Land is the real estate arm of one of the conglomerate companies JG Summit Holdings, Inc.(JGS:PHL). Robinson Land is engaged in the development and operation of shopping malls and hotels, office buildings, residential condominiums, and residential housing projects in key cities and other urban areas.

Before its success as a real estate developer in the country, Robinsons Land’s only focus was developing shopping malls in Metro Manila in the 1980s. As the popularity of malls as the go-to place for leisures rose, the company decided to open additional malls in other places outside the metro.

Robinsons Land was able to expand its mall footprint outside the country such as China, Hong Kong, and the U.K.

The firm’s expansion did not stop there. Robinsons Land saw the growing demand for business process outsourcing (BPO) companies in the country, which motivated Robinsons Land to start developing office buildings. Then, with the soaring demand for hotels and condominiums, Robinsons Land would soon add hotel operation and residential properties to its revenue sources.

However, like other companies, Robinsons Land stock price was dragged down by COVID-19 concerns. Specifically in March, its stock price deteriorated by more than 30%.

There are a number of factors as to why investors have been anxious about the company. First, the firm has delayed its plans to launch PHP 20 billion worth of new residential projects in 2020.

Second, China and the U.K., the overseas markets that the company is operating in, are areas that have been similarly impacted by the pandemic.

Third, rental collections from both malls and building offices were cancelled, while the company issued refunds to its hotel guests amid travel restrictions.

Although these short-term headwinds remain a concern, the relaxing of community quarantine restrictions in H2 2020 will help in the company’s recovery. Still, investors might remain worried about the firm’s profitability, especially since as-reported metrics have painted Robinsons Land as a low-profitability firm in the past.

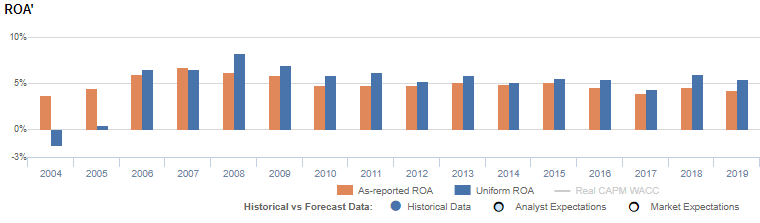

Specifically, as-reported metrics suggest that the company posted a 4% ROA in 2019. Meanwhile, when looking at the Uniform metrics, earning power is actually higher at 6%, which is above the cost of capital.

One of the distortions of the said discrepancy is due to Philippine Financial Reporting Standards (PFRS) accounting for interest expense.

According to PFRS, interest expense can be classified as an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully always a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

For example in 2019, Robinsons Land recognized an interest expense of PHP 1.1 billion, 12% of as-reported net income of PHP 8.7 billion. When we add the PHP 1.1 billion back to earnings along with many other necessary adjustments made, it leads to a 6% Uniform ROA in 2019, higher than as-reported ROA of 4%.

Robinsons Land’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think Robinsons Land’s profitability has been weaker than real economic metrics have highlighted in the past fourteen years.

In reality, Robinsons Land’s true profitability has been higher than as-reported ROA since 2006. Specifically, Uniform ROA was 6% in 2019, but as-reported ROA was only 4% that year.

After improving from 4% in 2004 to 7% in 2007, as-reported ROA gradually declined to 4% in 2017. Then, as-reported ROA improved to 5% in 2018, before fading back to 4% in 2019.

Meanwhile, after expanding from negative levels in 2004 to a peak of 8% in 2008, Uniform ROA gradually contracted to 4% in 2017, before recovering to 6% levels in 2018-2019.

Robinsons Land’s earnings margin is weaker than you think

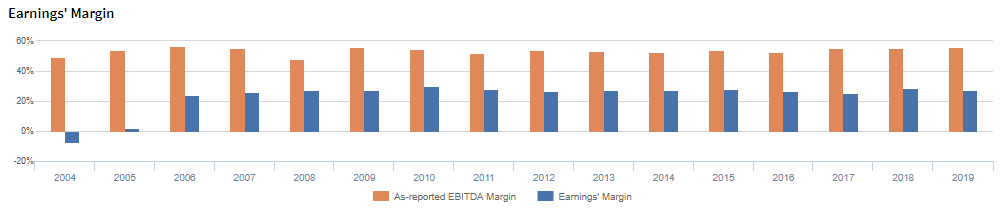

Strength in Uniform ROA has been generally offset by trends in Uniform earnings margin. In fact, as-reported margins have been higher than Uniform margins in each of the past sixteen years.

As-reported margins improved from 49% in 2004 to 56% in 2006, before fading to 48% in 2008 and subsequently recovering to 52%-56% levels through 2019.

Meanwhile, Uniform margins rose from -7% in 2004 to 30% in 2010, before compressing to 26% in 2017 and rebounding to 28% in 2019.

Looking at the firm’s margins alone, as-reported metrics are making the firm appear to be a more cost efficient business than is accurate.

SUMMARY and Robinsons Land Corporation Tearsheet

As the Uniform Accounting tearsheet for Robinsons Land highlights, it trades at a Uniform P/E of 21.1x, below the global corporate average of 25.2x but around its historical average of 22.2x.

Low P/Es require low EPS growth to sustain them. In the case of Robinsons Land, the company has recently shown a 6% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Robinsons Land’s sell-side analyst-driven forecast calls for a 34% Uniform EPS decline in 2020 before a 45% Uniform EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Robinsons Land’s PHP 21.0 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 2% each year over the next three years and still justify current valuations. What sell-side analysts expect for Robinsons Land’s earnings growth is below the requirement in 2020 but above the requirement in 2021.

Furthermore, the company’s earning power is near the long-run corporate average, and cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Robinsons Land’s Uniform earnings growth is above peer averages, but the company is below peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com